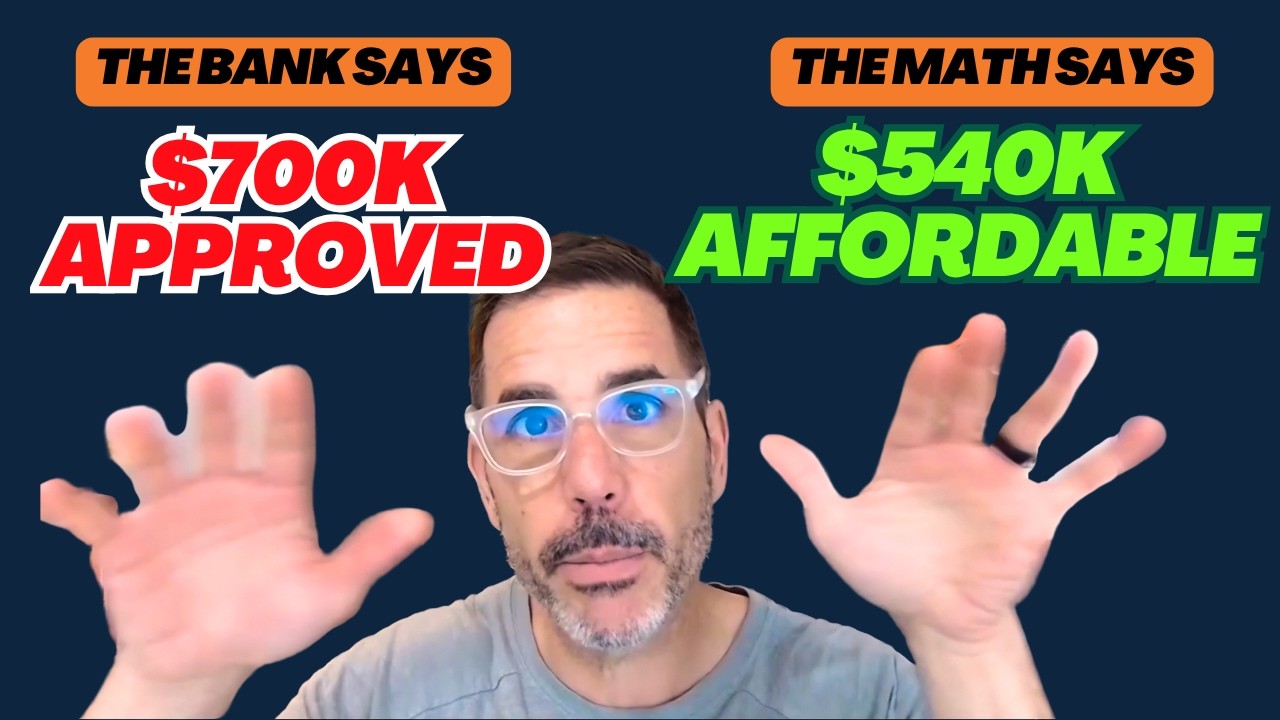

Getting pre-approved for a mortgage doesn’t always guarantee you’ll make it to the closing table. Imagine being just days away from closing on your dream home, only to find out your loan approval is in jeopardy. Unfortunately, this happens more often than most buyers realize, and it’s often caused by income, asset, or documentation issues that weren’t properly reviewed upfront. This video explains why some homebuyers experience last-minute mortgage delays or loan denials, even after receiving a pre-approval letter. You’ll learn what underwriters are really looking for and how to avoid surprises before closing.

In this video you’ll learn:

Why mortgage pre-approval is not the same as final loan approval

How bonuses, commissions, overtime pay, RSUs, rental income, and self-employment income are evaluated

Why variable income requires deeper analysis during underwriting

What documentation is needed when converting your current home into a rental property

Common reasons mortgage closings get delayed at the last minute

Questions every buyer should ask their lender before making an offer

How proper upfront loan review can help prevent stress, delays, and unexpected denials

Whether you’re a first-time homebuyer, relocating, or purchasing a new home while keeping your current property as a rental, understanding these requirements can help you avoid costly surprises and keep your transaction on track. Watch until the end to learn how experienced lenders review income, assets, tax returns, rental property documentation, and other key factors before underwriting begins.

Schedule a consultation: https://mortgage-maestro.com/contact/

Explore more videos on building wealth through real estate and making smarter home financing decisions.

⬇️⬇️⬇️⬇️⬇️⬇️⬇️

📌 *Are you looking to buy a home in Colorado, California, Texas, Wyoming, or Florida? Contact us to get started: https://mortgage-maestro.com/contact/

⬆️⬆️⬆️⬆️⬆️⬆️⬇️

👇Subscribe to my channel for more videos like this👇

https://www.youtube.com/@mortgagemaestro

⬇️⬇️⬇️⬇️⬇️⬇️⬇️

We're a veteran-owned, top-rated independent mortgage broker servicing Colorado, California, Wyoming, Texas, and Florida. Our mission is to empower you to build wealth through real estate, with a focus on expert advice and education on mortgages.

Whether you're a first-time home buyer interested in house hacking or real estate investing, our storytelling approach will guide you through every step of the process.

We upload videos regularly. SUBSCRIBE to get regular updates on mortgage rates, market trends, and invaluable insights to help you make informed decisions about your most significant asset.

⬆️⬆️⬆️⬆️⬆️⬆️⬇️

RAY WILLIAMS

Mortgage Maestro Group (NMLS #1838215)

🏢 387 N, Corona St #646, Denver, CO 80218

📞 (303) 779-0591

📧 [email protected]

#MortgageApproval #MortgagePreApproval #HomeBuyingTips #MortgageUnderwriting #LoanApproval #MortgageDenied #FirstTimeHomeBuyer #HomeBuyingProcess #MortgageTips #RealEstateInvesting