Did you know that mortgage insurance helps lots of people buy homes, even if they don’t have a big chunk of money saved up? It’s like a safety net for lenders, making it possible for folks with smaller down payments to get approved for home loans.

Over the last 66 years, private mortgage insurance (PMI) has helped over 38 million people become homeowners. These are folks who didn’t have enough money for a 20 percent down payment on a regular home loan.

Your mortgage is a really big deal and one of the most important financial decisions you’ll ever make. Owning a home is a big part of the American dream for many people. Because mortgages involve a lot of money, lenders do a few things to make sure their loans are safe.

What is Mortgage Insurance?

Mortgage insurance is like a safety net for lenders. If a borrower can’t make their payments, this insurance kicks in to cover the lender’s losses. Because of this protection, lenders can offer loans to people who might not otherwise qualify.

Normally, lenders want a big down payment, like 20%, to make sure the borrower is serious about paying back the loan. But with mortgage insurance, borrowers who can’t afford a big down payment still have a chance to buy a home.

There are different types: private mortgage insurance (PMI) for regular loans and mortgage insurance premium (MIP) for FHA loans.

Types of Mortgage Insurance

Private Mortgage Insurance (PMI)

Private mortgage insurance (PMI) is mostly for regular home loans. You pay a fee every month for PMI. This fee can be between 0.1% to 2% of what you owe each year.

There are four kinds of Private Mortgage Insurance (PMI):

- Monthly Payment: You pay a little bit extra every month along with your mortgage.

- One-Time Payment: You pay the insurance all at once when you get your mortgage, or you add it to your mortgage.

- Split Payment: You pay some of the insurance upfront and some every month.

- Lender Pays: The lender includes the insurance cost in your mortgage interest rate or the fee to start your mortgage.

Mortgage Insurance Premium (MIP)

Similar to PMI, it’s premium (also known as MIP) is required for borrowers using loans backed by the Federal Housing Administration (FHA).

FHA loans might only need a 3.5% down payment. But unlike PMI, MIP is mandatory for all FHA loans, no matter the down payment size. When you take out an FHA loan, you’ll have to pay an upfront its premium (which you can add to your loan) and an annual premium as part of your mortgage payments.

With PMI, you can stop paying it when you’ve built up enough equity in your home. However, to stop paying MIP, you’ll need to refinance your FHA loan to a conventional mortgage. If you put down at least 10% with an FHA loan, you’ll pay MIP for 11 years. But if your down payment is less than 10%, you’ll have to keep paying MIP for the entire time you have the loan.

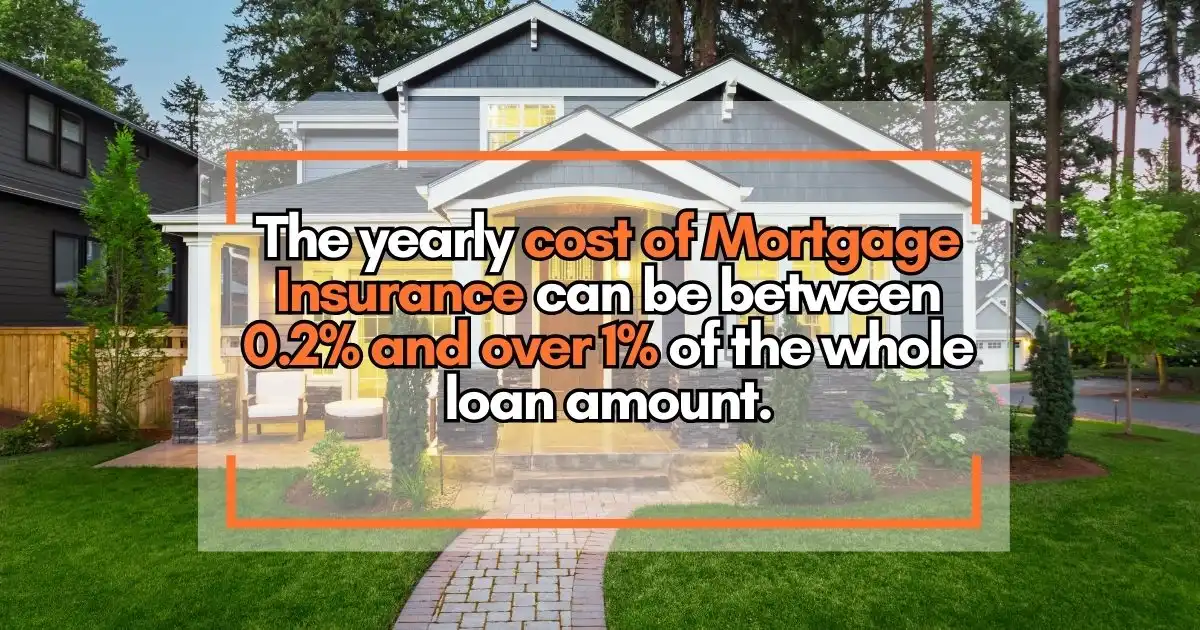

How Much Does It Cost?

The yearly cost of mortgage insurance can be between 0.2% and over 1% of the whole loan amount. It changes depending on things like:

- The type of loan you have

- How much of the loan is compared to the value of your house

- Your credit score

Usually, you pay this cost in equal parts each year, along with your regular monthly mortgage payment.

Pros And Cons Of Mortgage Insurance

Before you decide if getting mortgage insurance is a good idea for you, there are a few things you should think about. When you’re ready to buy a house, make sure you think about the good things and the not-so-good things carefully.

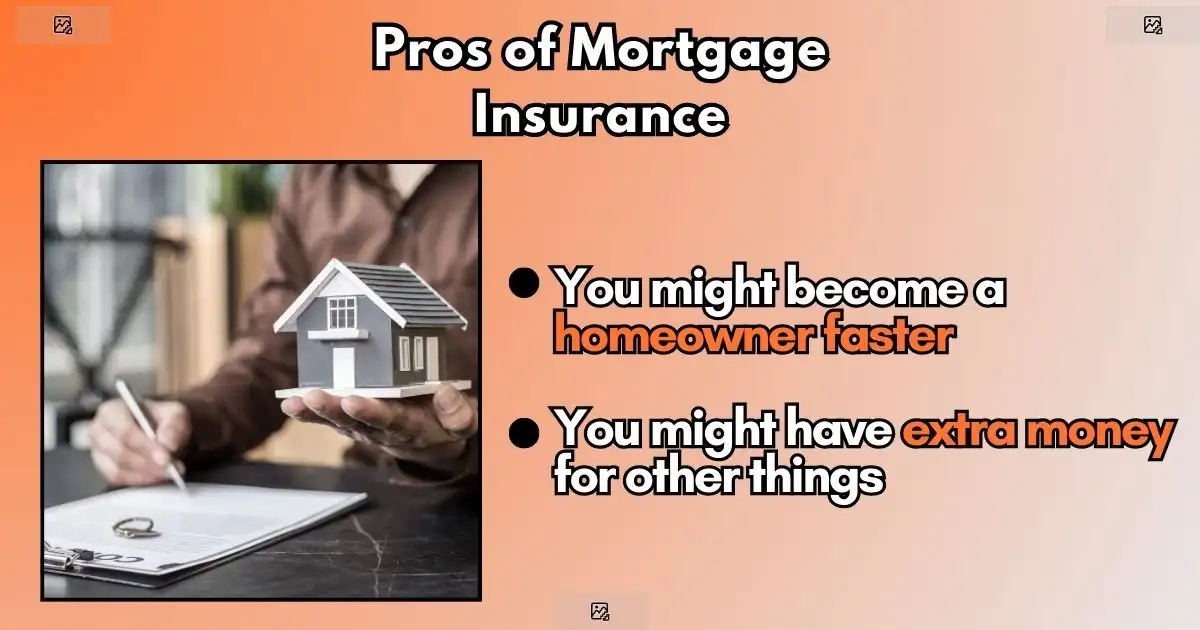

Pros of Mortgage Insurance

PMI or MIP can be good in certain cases. Here are the benefits:

- You might become a homeowner faster. Paying PMI or MIP means you don’t have to wait to save a lot of money to buy your home.

- You might have extra money for other things. Instead of using all your money for a big down payment, you can use it for fixing up your home or other things you need.

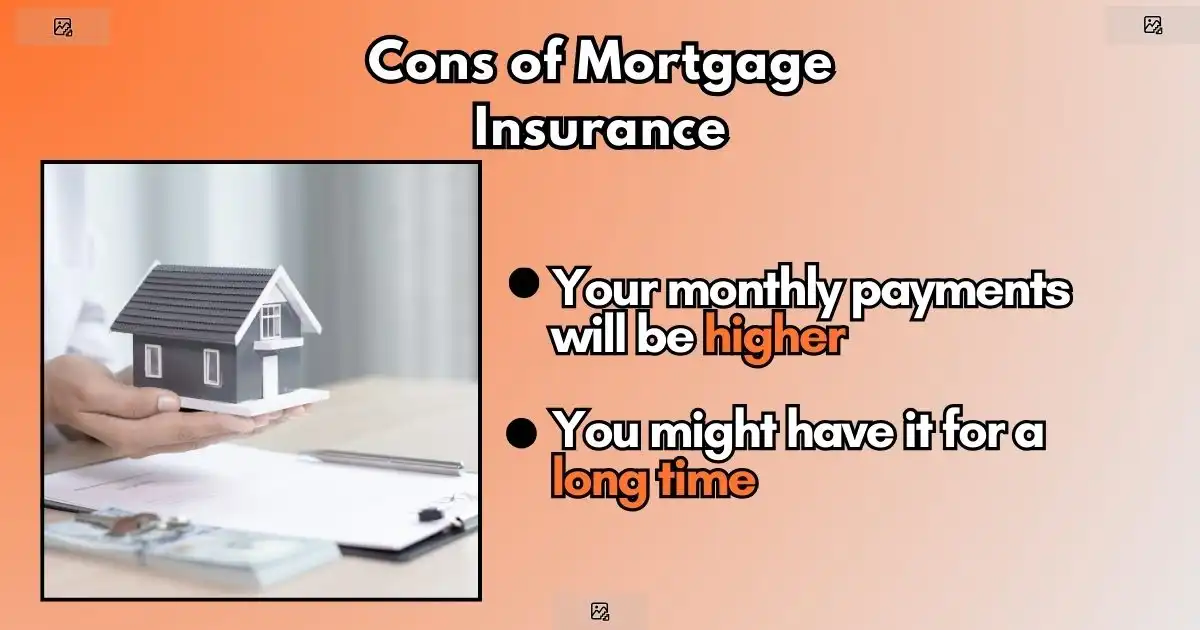

Cons of Mortgage Insurance

Mortgage insurance might not always be in your favo r when purchasing a home. Consider these downsides:

- Your monthly payments will be higher. Some types will increase your monthly mortgage payment.

- You might have it for a long time. With certain types of mortgage insurance, like PMI, you can only cancel it after you’ve built up at least 20% equity in your home. But it won’t automatically stop until you have 22% equity. With other types, like MIP, you might have to keep paying for a set number of years or for the entire life of the loan, depending on how much you put down. You can cancel MIP by refinancing your mortgage into a different type.

PMI vs. MIP

If you’re getting a regular mortgage and don’t put down much money, you’ll have to pay PMI. But if you’re getting an FHA loan, you’ll probably have to pay MIP instead. Let’s see how they both work:

Private Mortgage Insurance (PMI)

People who get conventional mortgages and can only put down between 3% and 19.99% usually need to get PMI. These borrowers are often buying their first home and not refinancing. They might have more debt compared to their income and lower credit scores than people who don’t need PMI, according to the Urban Institute.

Mortgage Insurance Premiums (MIP)

Borrowers who get a loan backed by the FHA need to pay an MIP. The main reason for this is that it might be the only way they can qualify for a home loan. According to the Urban Institute, FHA borrowers usually have lower credit scores and more debt compared to those who pay PMI on conventional loans.

The percentages change from year to year, but overall, around 30% of borrowers with guaranteed loans or pay MIP. Another 42% pay PMI, and the remaining 30% use a loan program from the Department of Veterans Affairs (VA), which doesn’t require PMI or MIPs.

If you get a loan backed by the U.S. Department of Agriculture (USDA), you’ll need to pay a 1% upfront loan guarantee fee and a monthly mortgage insurance fee of 0.35% of the loan amount.

Significance And Considerations

It helps protect lenders and borrowers. For lenders, it lowers the risk of losing money if borrowers can’t pay back their loans, so they can lend to more people. For borrowers, it means they can get a loan with a smaller down payment.

But borrowers need to think about the costs and rules. The insurance premiums add to the total cost of the loan, making monthly payments higher. So, borrowers should look into ways to lower or get rid of these premiums, like putting down more money upfront or refinancing later on when they owe less compared to the home’s value.

Your Dream Home With Mortgage Maestro Group

Getting a home is a big deal. Our team is here to support you in finding the perfect mortgage for you. If you’re trying to understand mortgage insurance and want to know about low down payment choices, come to Mortgage Maestro Group.

Our team is ready to help you with clear advice that fits your needs and money plans.For details and low down payment options, chat with one of our team members Mortgage Maestro Group.

Final Thoughts

Mortgage insurance makes homeownership more accessible by allowing borrowers to qualify for loans with smaller down payments. It comes in two types: PMI for regular loans and MIP for FHA loans. While it helps buyers enter the housing market sooner, it also means higher monthly payments and potentially longer payment periods.

Understanding the costs and benefits is important in making an informed decision on whether to opt.

FAQs

What idoes it mean?

A type of insurance that protects lenders in case a borrower defaults on their mortgage loan.

Why do I need mortgage insurance?

If you’re unable to make a down payment of at least 20% on your home, lenders often require to protect themselves against potential losses.

How does mortgage insurance work?

If you default on your mortgage payments, the insurance company pays the lender a portion of the outstanding loan balance, reducing the lender’s financial risk.

What types of mortgage insurance are there?

There are two main types: PMI for conventional loans and MIP for government-backed loans like FHA loans.

Mortgage Maestro Group – NMLS #1838215