2026 Ultimate Guide to Alternative Mortgage Options: Asset-Based, Crypto-Backed, Investor, Self-Employed, Move-Up, and VA Loans

Welcome to the financial landscape of 2026. The days when a standard W-2 and a 740 credit score were the only keys to unlocking the door to homeownership are long behind us. As the economy has shifted toward decentralized finance, gig-economy dominance, and diverse investment portfolios, the mortgage industry has evolved to meet borrowers where they are.

For high-net-worth individuals, cryptocurrency investors, self-employed entrepreneurs, and real estate moguls, traditional lending guidelines often fail to capture the full picture of financial health. If you have significant assets but minimal taxable income, or if your wealth is tied up in the blockchain, a conventional bank might turn you away. That is where alternative mortgage options and non-QM (Non-Qualified Mortgage) loans shine.

In this comprehensive guide, we will explore the sophisticated lending solutions available in 2026. From asset-based lending and crypto mortgages to DSCR loans for investors and bridge loans for move-up buyers, we will provide the blueprint for securing financing on your terms. Whether you are a veteran maximizing VA loans in 2026 or a business owner seeking no-doc mortgage solutions, this guide is your roadmap.

1. Introduction: The Evolving Mortgage Landscape in 2026

The mortgage market of 2026 is defined by flexibility. The rigid “check-the-box” underwriting of the past decade has given way to holistic financial assessment. Why? Because the modern borrower looks different. You might be a tech consultant paid in Ethereum, a retiree with a massive stock portfolio but no pension, or a real estate investor with ten rental properties.

Traditional income verification methods, such as tax returns, often penalize savvy borrowers who utilize legal tax deduction strategies. In response, alternative mortgage lenders have developed products that look at ability to repay through different lenses: liquid assets, cash flow, and equity.

In this guide, we will cover the key pillars of modern alternative lending:

Asset-Based Lending: Using your net worth, not your pay stub, to qualify.

Crypto-Backed Mortgages: Leveraging digital assets without triggering capital gains taxes.

Bank Statement Loans: The premier solution for the self-employed.

DSCR Loans: Financing investment properties based strictly on rental income.

Bridge Loans: Facilitating seamless transitions for move-up buyers.

VA Loans: The enduring power of zero-down financing for our military heroes.

If you are ready to explore these options, contact Ray Williams at [email protected] or call 13037790591 to discuss your specific scenario.

2. Asset-Based Lending and Crypto-Backed Mortgages

For high-net-worth individuals (HNWIs), showing a steady monthly income on a tax return can be difficult, or simply unnecessary. Asset-based lending (also known as asset depletion or asset dissipation loans) allows you to use your liquid assets to calculate a “derived” monthly income for mortgage qualification.

Asset-Based Lending: How High-Net-Worth Clients Qualify Without Traditional Income Verification

In 2026, asset-based lending has become a primary tool for retirees and wealthy individuals. The concept is simple: the lender takes your total eligible liquid assets (stocks, bonds, checking, savings, and retirement accounts) and divides them by a set term (usually 60 to 84 months) to create a phantom monthly income.

Example Calculation:

If you have $3,000,000 in a brokerage account and no job:

Lender Formula: $3,000,000 / 84 months = $35,714 per month in qualifying income.

Result: You easily qualify for a luxury home mortgage without submitting a single W-2 or tax return.

This method respects the fact that your wealth is your income. It eliminates the friction of explaining complex tax returns to an underwriter who may not understand sophisticated wealth management strategies.

Using Cryptocurrency Holdings as Assets to Secure a Mortgage in 2026

The integration of decentralized finance (DeFi) into mainstream lending is the biggest story of 2026. In the past, lenders viewed cryptocurrency as “volatile” and “untraceable.” Today, specialized lenders view Bitcoin, Ethereum, and major stablecoins as legitimate Tier 1 assets.

Eligibility Criteria for Crypto Mortgages:

Seasoning: Most lenders require the crypto to be in your wallet or exchange account for at least 30 to 60 days.

Audit Trail: You must provide a transaction history showing the source of funds (to comply with Anti-Money Laundering laws).

Asset Type: Blue-chip cryptos (BTC, ETH) are preferred; speculative altcoins may be discounted or disallowed.

Crypto Asset Mortgages: Turning Digital Investments into Homeownership

There are two distinct ways to leverage crypto for a home in 2026:

Crypto-as-Income (Asset Depletion): Similar to the stock portfolio example above, the lender values your crypto holdings (often applying a volatility buffer, e.g., counting 70% of the value) and divides it to create qualifying income.

Crypto-Collateralized Loans: You pledge your crypto assets as collateral for the loan. This is a no-doc mortgage structure where no income is verified. If the value of your crypto drops significantly, you may face a margin call, requiring you to deposit more crypto or pay down the principal.

Pros: You do not have to sell your crypto, avoiding a taxable event (capital gains). You maintain upside potential if the coin value increases.

Cons: Volatility risk. High interest rates compared to conventional loans.

Asset-Based Mortgages vs. Income-Based: Which Fits High-Asset Borrowers Best?

If you have a high net worth but low taxable income, asset-based is superior. However, if you have a high salary and high assets, an income-based loan might offer a slightly lower interest rate. The choice comes down to documentation. Asset-based loans are low-friction; they require statements, not tax returns. For privacy-conscious borrowers in 2026, this is a premium feature worth paying for.

No-Doc Mortgage Options for Entrepreneurs and Freelancers

True “No-Doc” loans (No Income, No Employment, No Asset) are rare and often predatory. However, “No-Income-Verification” loans are legitimate. These rely heavily on credit score (usually 700+) and down payment (usually 20-30%). The lender assumes that if you have significant skin in the game and a history of paying debts, you are a safe bet regardless of your current employment status.

3. Mortgage Solutions for Self-Employed Borrowers

The gig economy and entrepreneurship define the workforce of 2026. Yet, the tax code incentivizes business owners to write off expenses to lower their tax liability. This creates a paradox: you are wealthy in reality, but “poor” on paper. Self-employed mortgage solutions bridge this gap.

Bank Statement Loans: The Best Option for Self-Employed Borrowers in Today’s Market

Bank statement loans are the gold standard for business owners. Instead of looking at the “Adjusted Gross Income” on line 31 of your tax return, lenders look at the gross deposits entering your business or personal bank accounts.

How it Works:

12-Month or 24-Month Review: You provide bank statements for the last 12 to 24 months.

Revenue Calculation: The lender totals your deposits. For business accounts, they apply an expense factor (typically 50%, though this varies by industry type) to estimate net income.

Example: You deposit $500,000 into your business account annually. The lender assumes 50% overhead. Your qualifying income is $250,000.

This usually results in a qualifying income 3x to 5x higher than what appears on tax returns.

Self-Employed Mortgage Approval: Proven Strategies That Work in 2026

To ensure approval for a self-employed mortgage, follow these strategies:

Separate Finances: strictly keep business and personal funds separate. Co-mingling funds complicates the underwriting process.

Expense Factor Letters: If your business has low overhead (e.g., a digital consultant working from home), have your CPA write a letter stating your expense ratio is only 20% rather than the standard 50%. This boosts your qualifying income significantly.

Maintain High Credit: Since you aren’t providing tax returns, your credit score is your primary trust signal. Aim for 720 or higher for the best rates.

4. Financing Options for Real Estate Investors

For real estate investors building portfolios in 2026, personal income is irrelevant. The property should pay for itself. This philosophy is the foundation of investment property financing via DSCR loans.

Top Mortgage Solutions for Real Estate Investors Building Portfolios

Investors in 2026 are moving away from Fannie Mae/Freddie Mac conventional loans, which cap the number of financed properties (usually at 10) and require extensive personal DTI (Debt-to-Income) calculations. Instead, they utilize:

DSCR Loans: Based on property cash flow.

Portfolio Loans: Financing multiple properties under one loan (blanket mortgage).

Fix-and-Flip Loans: Short-term, hard money financing for renovation projects.

DSCR Loans Explained: Financing Investment Properties with Rental Income

DSCR stands for Debt Service Coverage Ratio. It is a simple calculation:

Gross Rental Income / Total Monthly Mortgage Payment (PITI) = DSCR Ratio.

Ratio > 1.0: The property is cash-flow positive. (e.g., Rent is $2,000, Mortgage is $1,500. DSCR = 1.33). This is a safe loan.

Ratio = 1.0: Breakeven.

Ratio < 1.0: Negative cash flow. Some aggressive lenders in 2026 still fund these (No-Ratio loans) if the borrower has significant reserves and a high down payment (30%+).

Why DSCR Wins: No employment verification. No tax returns. You can close in the name of an LLC to protect your personal liability. You can scale infinitely because the loans do not affect your personal DTI ratio.

Real Estate Investor Mortgages: Non-Owner-Occupied Financing Options

When financing non-owner-occupied properties, lenders assess the “lease” vs. “short-term rental” potential. In 2026, with the maturity of the Airbnb/VRBO market, many lenders will use AirDNA data or short-term rental projections rather than long-term lease agreements to calculate the DSCR. This is crucial for investors buying vacation rentals in high-demand areas where nightly rates far exceed monthly rent.

5. Move-Up Buyer Strategies

The “Move-Up” market is challenging. You have a home with equity, but you need to buy the new home before you sell the old one to avoid moving twice. In competitive markets, making an offer “contingent on the sale of your current home” is a recipe for rejection.

Move-Up Buyer Guide: How to Upgrade Your Home Without Financial Stress

The key to upgrading without stress is liquidity. You need access to the equity in your current home before it sells. Traditional HELOCs (Home Equity Lines of Credit) can be difficult to obtain once your home is listed for sale. This is where bridge loans enter the equation.

Bridge Loans for Move-Up Buyers: Buy Your Next Home Before Selling the Current One

A bridge loan is short-term interim financing that “bridges” the gap between buying a new home and selling your old one.

Mechanics of a Bridge Loan:

The lender gives you a loan against the equity of your current home.

You use these funds for the down payment on the new home.

You now own two homes temporarily.

You have a grace period (usually 6 to 12 months) to sell your old home.

Once the old home sells, the proceeds pay off the bridge loan.

Seamless Home Upgrades: Financing Strategies for Move-Up Buyers in Competitive Markets

To win in 2026, consider the Cross-Collateralization Strategy. Some lenders will place a lien on both properties, allowing you to finance 100% of the new purchase without a cash down payment. This makes your offer as strong as a cash offer.

Risk Mitigation: Ensure you have a realistic valuation of your current home. If the market dips and your home sells for less than the bridge loan amount, you are responsible for the difference. Always keep 6 months of reserves to cover payments on both homes if the sale takes longer than expected.

6. VA Loans for Veterans and Active-Duty Military

The VA loan remains the most powerful mortgage product on the market in 2026. Backed by the Department of Veterans Affairs, it offers benefits that no commercial loan can match.

VA Loan Success Stories: Maximizing Benefits for Veterans and Active-Duty Military

We have seen veterans in 2026 use their VA entitlement to build wealth, not just buy a home. By purchasing a multi-unit property (up to 4 units), a veteran can live in one unit and rent out the other three. The rental income can often cover the entire mortgage, allowing the veteran to live expense-free while building equity. This is the ultimate “house hack.”

VA Loans in 2026: Updated Benefits and Zero-Down Opportunities for Veterans

Key Updates for 2026:

No Loan Limits: Veterans with full entitlement can borrow as much as a lender is willing to approve without a down payment, provided they can afford the payments. We regularly close $1.5M+ VA loans with 0% down.

Funding Fee Adjustments: For veterans with a service-connected disability rating of 10% or higher, the VA Funding Fee is completely waived. This saves thousands of dollars at closing.

Restoration of Entitlement: Veterans who have paid off a previous VA loan can restore their entitlement to buy again with 0% down, making it a lifetime benefit.

7. Comprehensive FAQ Section

Below are detailed answers to common questions regarding alternative lending in the 2026 market.

1. What are the disadvantages of asset-based lending?

The primary disadvantages of asset-based lending include higher interest rates compared to conventional conforming loans (typically 0.5% to 1.5% higher) and higher down payment requirements (often 20% to 30%). Additionally, because these loans are “Non-QM” (Non-Qualified Mortgages), they are often held in lender portfolios rather than sold to Fannie Mae, meaning the terms (such as prepayment penalties) can be stricter. Borrowers must also have substantial liquid assets; illiquid assets like real estate or private equity usually do not count toward the income calculation.

2. Is asset-based lending the same as mortgage?

Yes, asset-based lending is a type of mortgage. It refers to the specific underwriting method used to qualify for the loan. The end result is the same: a lien is placed on the property, and you make monthly payments. The difference lies solely in how the lender verifies your ability to repay the loan—using accumulated assets rather than monthly earned income.

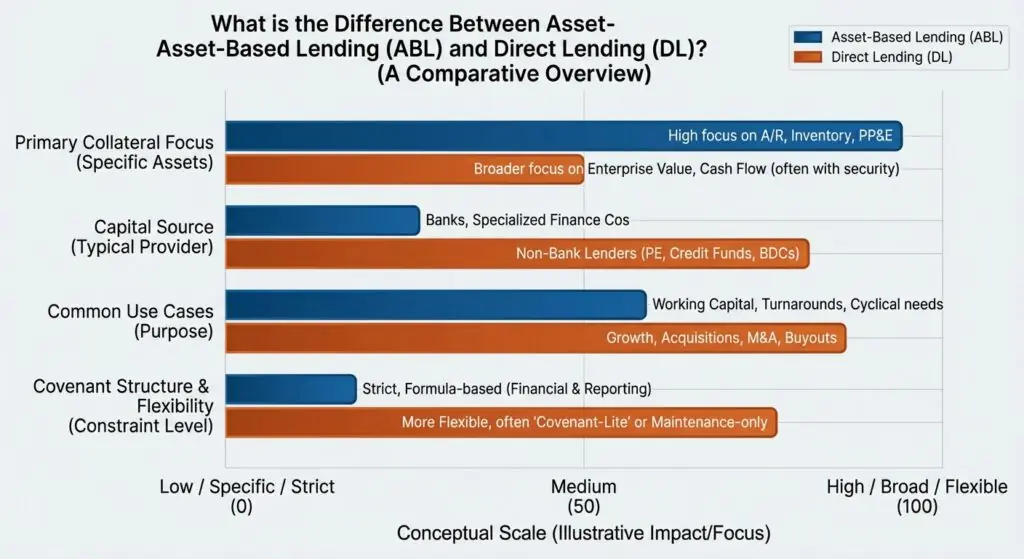

3. What is the difference between asset-based lending and direct lending?

These terms refer to different aspects of the process. Asset-based lending describes how you qualify (using assets). Direct lending describes who gives you the money. A direct lender originates the loan with their own funds. You can get an asset-based loan from a direct lender. Conversely, a mortgage broker (who is not a direct lender) can also arrange an asset-based loan for you by connecting you with a lender.

4. What are the types of asset-based loans?

There are three main types:

1. Asset Depletion/Dissipation: The lender divides your total liquid assets by a term (e.g., 60 months) to calculate phantom income.

2. Pledged Asset Loans: You pledge assets (like stocks) as collateral to the bank to secure the loan, often allowing for higher Loan-to-Value (LTV) ratios.

3. Securities-Based Lines of Credit (SBLOC): While not a traditional mortgage, this allows you to borrow against your portfolio to buy a home with cash, then refinance later.

5. Can you use crypto as collateral for mortgage?

6. Does crypto count as an asset for a mortgage?

Yes. Even for non-crypto specific loans, cryptocurrency can often count toward your “reserves” requirement. However, most lenders require the crypto to be liquidated into USD or a stablecoin and seasoned in a US bank account for 30 to 60 days before closing to be used for the down payment.

7. Do mortgage lenders care about crypto?

Traditional lenders (banks) are still wary of crypto due to volatility and anti-money laundering (AML) concerns. However, Non-QM and alternative lenders actively court crypto investors. They care about the audit trail—you must be able to show where the money came from and that it wasn’t derived from illegal activities.

8. Do banks accept crypto as collateral?

Most traditional retail banks (e.g., Chase, Wells Fargo) do not directly accept crypto as collateral for a mortgage in 2026. This service is primarily offered by specialized fintech mortgage lenders, private banks, and wealth management firms serving high-net-worth clients.

9. Which bank is best for real estate investors?

There is no single “best” bank, but investors typically find the best success with local community banks and Non-QM lenders rather than large national banks. Local banks offer “portfolio loans” with flexible terms, while Non-QM lenders specialize in DSCR loans that national banks typically do not offer.

10. Which lender is best for investment property?

The best lender for investment property is a DSCR Lender. These lenders focus solely on the property’s cash flow rather than your personal income. Contact Ray Williams at Mortgage Maestro for access to top-tier DSCR lending networks that offer competitive rates and high leverage.

11. What income do you need for a $600000 mortgage?

Assuming a 2026 interest rate of roughly 6.5%, property taxes, and insurance, a $600,000 mortgage payment (principal and interest) is approximately $3,800/month. Adding taxes and insurance might bring this to $4,800/month. Lenders typically look for a Debt-to-Income (DTI) ratio of 43% or lower. Therefore, you would need a monthly gross income of roughly $11,200, or an annual salary of approximately $135,000, assuming you have no other major debts.

12. What is the best software for real estate investing?

In 2026, the top software for investors includes DealCheck for analyzing potential returns, Stessa for portfolio accounting and tracking, and PropStream for sourcing off-market leads and analyzing market data.

13. Can I get a loan with just bank statements?

Yes. This is called a Bank Statement Loan. It is designed for self-employed borrowers. You do not provide tax returns or W-2s; the lender analyzes 12 to 24 months of bank deposits to determine your income.

14. How do I get a bank statement loan?

To get a bank statement loan, you must:

1. Be self-employed for at least two years (verified by a business license or CPA letter).

2. Provide 12 or 24 months of business or personal bank statements.

3. Have a credit score typically above 660.

4. Have a down payment of at least 10-20%.

Contact a specialized mortgage broker like Ray Williams, as these loans are not available at standard banks.

15. What are the cons of a bank statement loan?

The cons include higher interest rates (usually 1-2% higher than conventional loans), larger down payment requirements, and stricter credit score requirements. Additionally, you cannot use this loan type if you are a W-2 employee; it is exclusively for the self-employed.

16. What is the minimum down payment for a bank statement loan?

The minimum down payment is typically 10% for borrowers with excellent credit (740+). However, most lenders prefer or require 20% down to secure a competitive interest rate and mitigate risk.

17. Can you get a mortgage if you are self-employed?

Absolutely. While traditional banks may make it difficult due to tax write-offs, the alternative lending market caters specifically to you through Bank Statement Loans, 1099 Loans, and P&L (Profit and Loss) Loans.

18. Is it harder to get a loan if you’re self-employed?

It is harder to get a traditional government-backed loan (Fannie Mae/FHA) because of the strict documentation requirements regarding taxable income. However, it is not harder to get a loan if you utilize Non-QM lenders who are specifically set up to underwrite self-employed borrowers based on real cash flow.

19. What do I need to show for a self-employed mortgage?

For a traditional loan: 2 years of tax returns (1040s and business returns).

For an alternative loan: 12-24 months of bank statements, a business license, and a letter from your CPA verifying your business ownership percentage and expense ratio.

20. How much do you have to earn to qualify for a $200,000 mortgage?

For a $200,000 mortgage at 6.5% interest, the monthly P&I payment is roughly $1,265. With taxes and insurance, estimate $1,600/month. To keep this under 43% of your income, you need a monthly gross income of roughly $3,700, or an annual income of $45,000.

21. Who qualifies for a bridging loan?

Qualifying for a bridge loan typically requires significant equity in your current home (usually you must have at least 20-30% equity remaining after the bridge loan is issued), a strong credit score (700+), and sufficient assets or income to handle the payments of the new home plus the bridge loan interest.

22. What are the downsides of a bridging loan?

The downsides include high interest rates (often 2% to 4% higher than standard mortgages), high closing costs (origination fees), and the risk of owning two homes simultaneously if your old home does not sell. This can create financial strain if the market slows down.

23. Who is the ideal candidate for a bridge loan?

The ideal candidate is a move-up buyer in a “hot” seller’s market who has substantial equity in their current home but limited liquid cash for a down payment. They need to make a non-contingent offer to win the new house and are confident their current home will sell quickly.

24. What is the typical interest rate on a bridging loan?

In the 2026 market, bridge loan rates typically range from 8% to 11%. While this is higher than a 30-year mortgage, remember that it is a short-term convenience product intended to be paid off within 6 to 12 months.

Ready to Explore Your Options?

The mortgage world in 2026 is vast and full of opportunities for those who know where to look. Whether you are leveraging your crypto portfolio, using bank statements to prove your business success, or investing in your next rental property, there is a loan product designed for you.

Do not let traditional banks dictate your financial future. Work with an expert who understands the full spectrum of alternative lending.

Contact Ray Williams today.

Email: [email protected]

Phone: 13037790591

Your Partner in Modern Mortgage Solutions.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates and guidelines are subject to change. Please consult with a qualified mortgage professional for your specific situation.