What Are Bank Statement and Stated-Income Loans?

If you are a self-employed professional, freelancer, or business owner in Denver, CO, securing a traditional home loan can sometimes feel like an uphill battle. Standard underwriting requires tax returns that might not accurately reflect your true purchasing power due to legitimate business write-offs. This is exactly where a bank statement mortgage comes into play.

Also known as stated-income loans or alternative documentation loans, a bank statement loan allows borrowers to qualify for a mortgage based on their actual cash flow rather than their net income reported to the IRS. Instead of providing W-2s or tax returns, you simply provide personal or business bank statements to verify your monthly income.

At Mortgage Maestro Group, we specialize in helping self-employed individuals navigate these unique financing options. Whether you are exploring a non-qualified mortgage (Non-QM) or looking for a self-employed alternative doc mortgage, our veteran-owned team is here to guide you to the right solution.

Exploring 12-Month, 24-Month, Asset-Based, and DSCR Loan Options

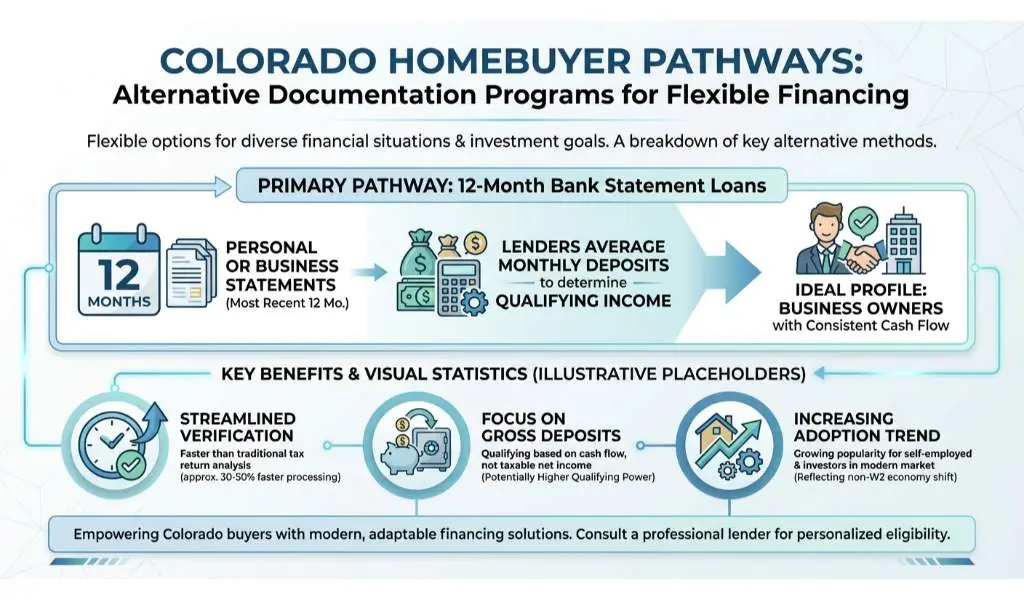

When applying for a bank statement loan, you have several flexible pathways depending on your financial situation and investment goals. Here is a breakdown of the most common alternative documentation programs available to Colorado homebuyers:

- 12-Month Bank Statement Loans: This option requires you to submit your most recent 12 months of personal or business bank statements. Lenders will average your monthly deposits to determine your qualifying income. It is ideal for business owners with consistent recent cash flow.

- 24-Month Bank Statement Loans: For those whose income might have seasonal fluctuations, a 24-month review provides a longer historical average. This often results in more favorable terms since it demonstrates long-term financial stability.

- Asset-Based Loans: Also known as asset depletion loans, this program allows you to qualify based on your liquid assets (like savings, investment accounts, or retirement funds) rather than your monthly income stream.

- DSCR Loans: Debt Service Coverage Ratio (DSCR) loans are designed specifically for real estate investors. Instead of looking at your personal income, the lender qualifies the property based on its potential rental income compared to the monthly mortgage payment.

If you have already been quoted for one of these products, do not settle immediately. We are experts at providing second opinions on bank statement loans. A quick review from our team can ensure you are getting the most competitive rate and the right portfolio or in-house underwritten mortgage for your specific needs.

| Loan Type | Target Borrower | Income Verification Method | Best Use Case |

|---|---|---|---|

| 12-Month Bank Statement | Self-Employed & Freelancers | 12 months of total deposits | Consistent recent business cash flow |

| 24-Month Bank Statement | Business Owners | 24 months of total deposits | Seasonal or fluctuating income |

| Asset-Based Loan | High Net Worth Individuals | Liquid assets divided over time | Retirees or buyers with large savings but low income |

| DSCR Loan | Real Estate Investors | Property rental income vs. debt | Expanding an investment portfolio without personal income verification |

Why Choose Mortgage Maestro Group for Your Bank Statement Loan

Securing a bank statement mortgage requires working with a broker who understands the nuances of self-employment and non-traditional income. As a top-rated, veteran-owned mortgage broker in Denver, CO, Mortgage Maestro Group has a proven track record of helping clients who were turned away by traditional banks.

Led by Ray Williams, our team takes the time to analyze your unique financial picture. We know that every business owner operates differently. That is why we offer a wide array of loan options to fit your exact circumstances. Whether you are buying a primary residence, a vacation home, or an investment property, we structure your stated-income loan for maximum success.

Remember, getting a second opinion is crucial in today’s market. We frequently help borrowers save money by finding better terms or more suitable alternative documentation programs after they have been denied or offered subpar rates elsewhere. Let us take the stress out of your mortgage journey.

Q1: What credit score is needed for a bank statement mortgage?

Generally, lenders look for a minimum credit score of 600 to 620 for bank statement loans, though higher scores will unlock the best interest rates and lower down payment requirements.

Q2: Can I use business bank statements instead of personal ones?

Yes, you can use either personal or business bank statements. If you use business statements, lenders typically apply an expense factor (often 50 percent) to determine your net qualifying income.

Q3: Do bank statement loans require a larger down payment?

Because stated-income loans carry slightly more risk for the lender, they usually require a minimum down payment of 10 to 20 percent, depending on your credit score and the specific loan program.

Q4: How long do I need to be self-employed to qualify?

Most lenders require you to have been self-employed or operating your business for at least two years to qualify for a bank statement mortgage.

Q5: Are interest rates higher on stated-income loans?

Interest rates for alternative documentation loans are typically slightly higher than conventional loans. However, getting a free second opinion from Mortgage Maestro Group can help ensure you receive the most competitive rate available.