What is a Cash-Out Refinance and How Does It Work?

If you are a homeowner in Denver, CO, you have likely seen your property value increase significantly over the past few years. A cash out refinance, also known as a cash-out mortgage, allows you to tap into that built-up equity. Instead of simply replacing your current mortgage with a new one of the same balance, you take out a new loan for more than you currently owe. The difference is paid to you in tax-free cash at closing.

Homeowners choose this financial strategy for a variety of reasons:

- Funding major home renovations or repairs

- Securing a debt consolidation mortgage to pay off high-interest credit cards

- Investing in a new business venture or a second property

- Covering college tuition or unexpected medical bills

Before you sign on the dotted line, it is critical to compare your options. We are experts at providing second opinions on cash-out refinance offers to ensure Denver homeowners get the most competitive rates and lowest fees possible.

Exploring Your Cash-Out Mortgage Options: Conventional, FHA, and VA

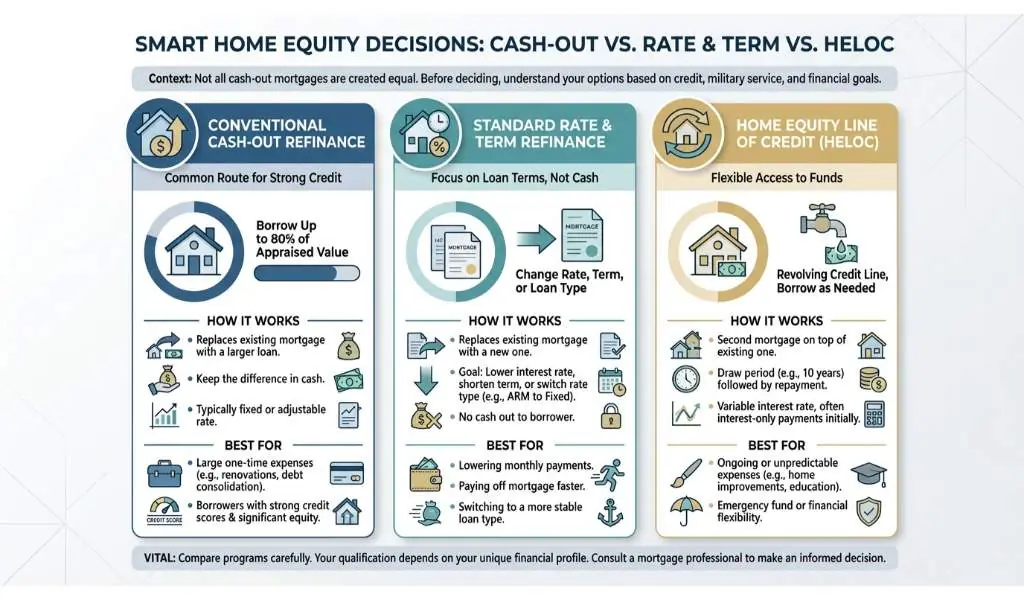

Not all cash-out mortgages are created equal. Depending on your credit score, military service, and financial goals, you may qualify for different loan programs. It is vital to understand these options before deciding between a cash out refinance, a standard rate and term refinance, or a home equity line of credit HELOC.

Conventional Cash-Out Refinance: This is the most common route for borrowers with strong credit. You can typically borrow up to 80 percent of your home’s appraised value. It is an excellent choice if you want to avoid upfront mortgage insurance premiums.

FHA Cash-Out Refinance: Backed by the Federal Housing Administration, this option is ideal for borrowers who might have lower credit scores or higher debt-to-income ratios. Like conventional loans, FHA guidelines generally allow you to access up to 80 percent of your home’s equity.

VA Cash-Out Refinance: As a veteran-owned Colorado mortgage broker, Mortgage Maestro proudly helps eligible veterans and active-duty service members utilize VA loans. The VA cash-out refinance is incredibly powerful, often allowing borrowers to access up to 90 percent or even 100 percent of their home’s value under certain lender guidelines.

| Loan Type | Maximum LTV (Loan-to-Value) | Typical Minimum Credit Score | Best For |

|---|---|---|---|

| Conventional | Up to 80% | 620+ | Borrowers with strong credit and high equity |

| FHA | Up to 80% | 580+ | Borrowers needing flexible credit requirements |

| VA | Up to 90% – 100% | 580+ (varies by lender) | Eligible Veterans and Active-Duty Military |

Why Get a Second Opinion on Your Cash-Out Refinance in Colorado?

Securing a new mortgage is one of the largest financial decisions you will make. Unfortunately, many homeowners accept the first offer they receive from their current lender without shopping around. Rates, closing costs, and loan terms can vary wildly from one institution to another.

At Mortgage Maestro, Ray Williams and his team specialize in analyzing existing loan estimates. We provide free, no-obligation second opinions on cash-out refinance offers. By reviewing your current estimate, we can often find ways to save you thousands of dollars over the life of the loan. Whether you are looking to consolidate debt, remodel your kitchen, or simply secure a better financial future, working with a top-rated, independent mortgage broker in Denver ensures you have a dedicated advocate in your corner.

Ready to explore your options? Give us a call at 303-779-0591 or email [email protected] to schedule your free consultation today.

Q1: What is the primary advantage of a cash out refinance?

The main advantage is the ability to access a large lump sum of your home’s equity at a mortgage interest rate, which is typically much lower than rates for personal loans or credit cards.

Q2: How does a cash-out mortgage differ from a HELOC?

A cash-out refinance replaces your existing primary mortgage with a completely new loan. A home equity line of credit HELOC is a separate, second mortgage that acts like a credit card tied to your home’s equity.

Q3: Can I use a cash out refinance for debt consolidation?

Yes. Using a debt consolidation mortgage strategy is very common. You can use the cash from your equity to pay off high-interest credit cards or auto loans, rolling all your debt into one lower monthly payment.

Q4: What are the loan-to-value limits for a VA cash-out refinance?

VA loans are highly beneficial for eligible veterans, typically allowing borrowers to access up to 90 percent or sometimes 100 percent of their home’s appraised value, depending on specific lender overlays.

Q5: Why should I get a second opinion on my refinance offer?

Lenders charge different interest rates and origination fees. Getting a free second opinion from an independent Denver mortgage broker like Mortgage Maestro ensures you are getting the absolute best deal available.