What is an FHA 203(k) Renovation Loan?

Finding the perfect home in the competitive Denver real estate market can be challenging. Often, the homes in your desired neighborhood might need a little TLC or a major overhaul. This is where the FHA 203k loan comes in. An FHA 203(k) Renovation Loan allows you to finance both the purchase (or refinance) of a house and the cost of its rehabilitation through a single mortgage.

Instead of taking out a standard FHA purchase loan and struggling to find separate financing for home repairs, this specialized program wraps everything into one manageable monthly payment. If you are comparing options, you might also consider a conventional renovation loan, but the FHA 203k Renovation program is often more accessible for buyers with lower credit scores or smaller down payments.

As a veteran-owned Colorado mortgage broker, Mortgage Maestro has extensive experience guiding Denver homeowners through this process. In fact, we are experts at providing second opinions on FHA 203k renovation loans to ensure you are getting the best terms possible.

Standard 203(k) vs. Limited 203(k): Which is Right for You?

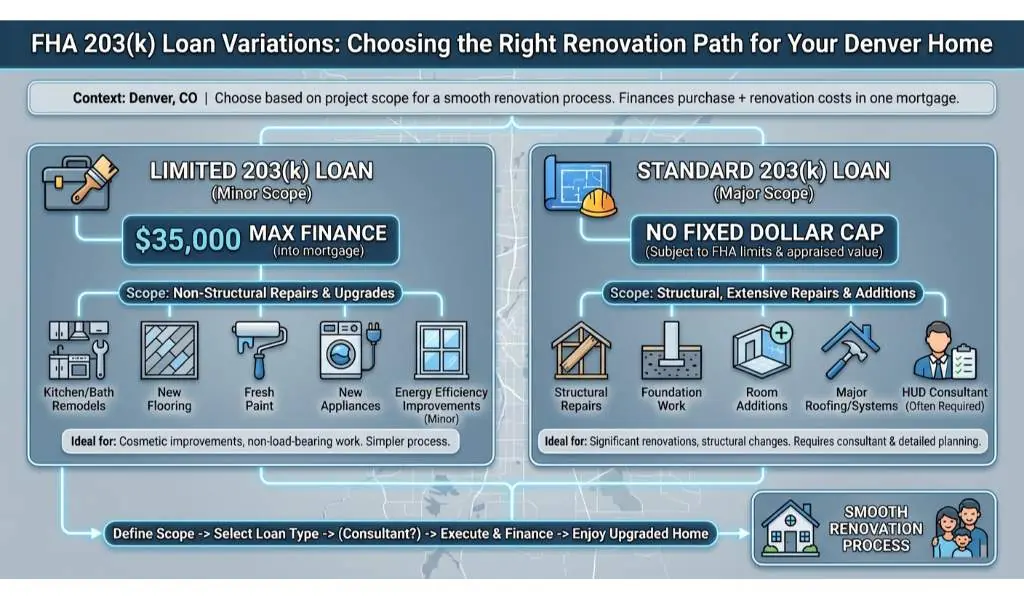

When applying for an FHA 203k loan, you will need to choose between two main variations based on the scope of your project. Understanding the difference is crucial for a smooth renovation process in Denver, CO.

- The Limited 203(k) Loan: This option is ideal for minor remodeling and non-structural repairs. It allows you to finance up to $35,000 into your mortgage to upgrade, improve, or repair your home. Projects like kitchen and bathroom remodels, new flooring, fresh paint, or new appliances fit perfectly here.

- The Standard 203(k) Loan: If your dream home requires structural alterations, room additions, or repairs exceeding $35,000, the Standard 203(k) is the right choice. This program requires the use of a HUD-approved 203(k) Consultant to oversee the project, ensuring the architectural and structural integrity of your Denver property.

Whether you are fixing up a historic home in Capitol Hill or updating a mid-century property in the suburbs, knowing which FHA 203k Renovation program fits your needs is the first step.

| Feature | Limited 203(k) | Standard 203(k) |

|---|---|---|

| Maximum Repair Amount | Up to $35,000 | No limit (subject to FHA loan limits) |

| Minimum Repair Amount | No minimum | $5,000 |

| Structural Repairs Allowed? | No | Yes |

| HUD Consultant Required? | No | Yes |

| Best For | Cosmetic updates, appliances, paint | Major additions, foundational work |

Why Get a Second Opinion on Your FHA 203k Renovation Loan?

Renovation loans are complex. Not all lenders have the specialized knowledge required to process an FHA 203k loan efficiently. Delays in underwriting or miscalculations in renovation costs can jeopardize your real estate transaction.

At Mortgage Maestro, we are experts at providing second opinions on FHA 203k renovation loans. If you are already working with a lender but feel unsure about the rates, fees, or timeline, Ray Williams and our team can review your loan estimate. As a trusted independent mortgage broker in Denver, CO, we offer transparency and top-tier advice. We often save homebuyers significant money and stress by identifying better loan structures or catching hidden fees.

Compliance Note: Mortgage Maestro NMLS#1838215. All loans are subject to underwriter approval. Equal Housing Opportunity.

Q1: What credit score is required for an FHA 203k loan?

Generally, a minimum credit score of 580 is required to qualify for the 3.5% down payment advantage of an FHA 203k loan.

Q2: Can I do the renovation work myself with an FHA 203k Renovation Loan?

No, you cannot perform the repairs yourself. All work must be completed by a licensed, insured, and approved general contractor.

Q3: Are luxury items like swimming pools covered under this loan?

No, the FHA 203k Renovation program does not allow funding for luxury items such as new swimming pools, outdoor fireplaces, or tennis courts.

Q4: How long does the renovation process take?

Under the Standard 203(k) and Limited 203(k) guidelines, renovations must typically begin within 30 days of closing and be completed within six months.

Q5: Can I use an FHA 203k loan for an investment property?

No, FHA loans are strictly for owner-occupied primary residences. You must intend to live in the home after the renovations are complete.