What is an Assumable Mortgage and How Does Mortgage Assumption Work?

If you are looking to buy a home in Denver, CO, you might be searching for creative ways to secure a lower interest rate. Enter the assumable mortgage, also known as a mortgage assumption. An assumable mortgage allows a homebuyer to take over the seller’s current mortgage terms. This means you inherit their interest rate, repayment period, and current principal balance.

In a housing market where interest rates fluctuate, taking over a loan with a historically low rate can save you thousands of dollars over the life of the loan. At Mortgage Maestro, we are experts at providing second opinions on assumable mortgages to ensure you are getting the best possible deal. Whether you are navigating a complex transaction or just want to explore your financing options, our veteran-owned independent brokerage is here to guide you.

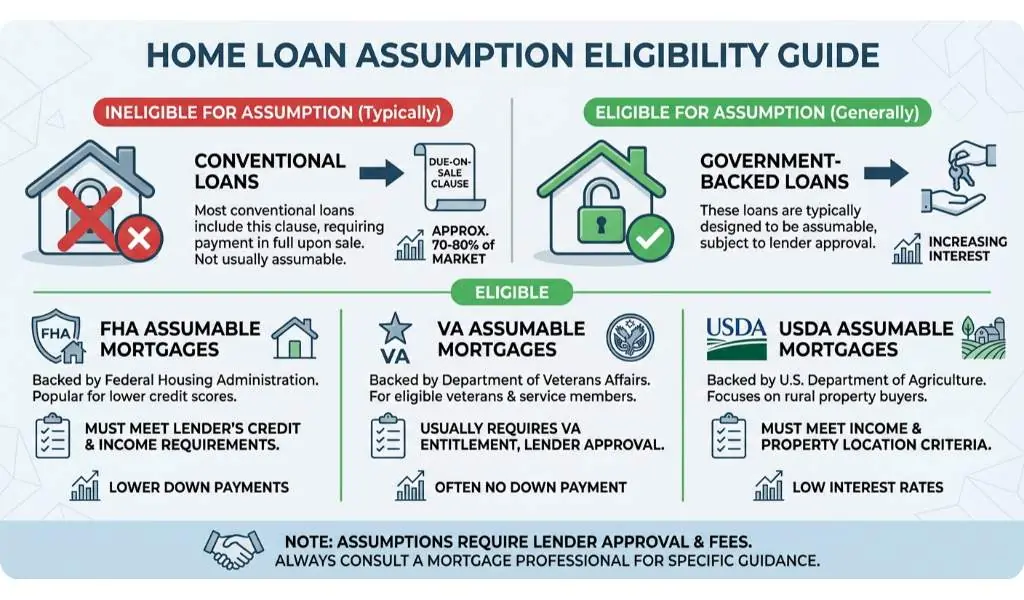

Types of Assumable Mortgages: FHA, VA, and USDA Loans

Not all home loans are eligible for a mortgage assumption. Conventional loans typically have a due-on-sale clause, making them ineligible. However, government-backed loans are generally assumable. Here is a breakdown of the three main types of government-backed assumable loans:

- FHA Assumable Mortgages: Backed by the Federal Housing Administration, these loans are popular for buyers with lower credit scores. If you are considering an FHA assumption, you must meet the lender’s credit and income requirements. You can learn more about FHA guidelines on our FHA purchase loan page.

- VA Assumable Mortgages: Department of Veterans Affairs loans offer incredible benefits. A unique feature of a VA assumable mortgage is that the buyer does not necessarily need to be a military veteran to assume the loan. However, the original veteran seller’s entitlement remains tied to the property unless the buyer is an eligible veteran who substitutes their own entitlement. For more details, visit our VA purchase loan resource.

- USDA Assumable Mortgages: Designed for rural and suburban homebuyers, USDA loans are also assumable. The new borrower must meet strict USDA income limits and property location requirements.

If an assumable mortgage does not perfectly align with your financial goals, you might also consider alternative strategies like a rate and term refinance down the road to secure better terms.

| Loan Type | Assumable? | Special Requirements |

|---|---|---|

| FHA Loans | Yes | Buyer must meet standard FHA credit and income qualifications. |

| VA Loans | Yes | Entitlement substitution is required to free up the seller’s VA benefits. |

| USDA Loans | Yes | Subject to USDA income limits and location eligibility rules. |

| Conventional Loans | Rarely | Typically contain a due-on-sale clause preventing assumption. |

Why Get a Second Opinion on Your Mortgage Assumption in Denver?

Navigating an assumable mortgage in the competitive Denver real estate market can be challenging. The process often involves a significant cash difference between the home’s purchase price and the remaining mortgage balance. This gap must be covered by a sizable down payment or secondary financing, which requires careful financial planning.

Because a mortgage assumption involves working directly with the seller’s original lender, the timeline and paperwork can be rigorous. This is exactly why getting a professional review is crucial. We are experts at providing second opinions on assumable mortgages. Ray Williams and the team at Mortgage Maestro will review your unique scenario, calculate your potential savings, and help you determine if the upfront cash requirements make sense for your long-term wealth-building strategy.

Q1: What is an assumable mortgage?

An assumable mortgage allows a buyer to take over the seller’s existing home loan, keeping the original interest rate, repayment terms, and remaining loan balance.

Q2: Are conventional loans assumable?

Generally, conventional loans are not assumable because they include a due-on-sale clause. Mortgage assumption is primarily available for government-backed loans like FHA, VA, and USDA loans.

Q3: Do I need good credit to assume an FHA loan?

Yes, the buyer must apply and qualify for the FHA assumable mortgage based on the original lender’s credit, debt-to-income ratio, and income requirements.

Q4: Can a non-veteran assume a VA loan?

Yes, a non-veteran can assume a VA loan. However, the original veteran seller will not get their VA entitlement back until the loan is paid in full, unless the buyer is a veteran who substitutes their own entitlement.

Q5: How can a Denver mortgage broker help with an assumption?

At Mortgage Maestro, we offer expert second opinions to evaluate if an assumable mortgage is your most cost-effective path to homeownership in Denver, CO, helping you weigh the pros and cons of the required down payment.