Understanding Condo Loans: Warrantable vs. Non-Warrantable Condos

Securing condo mortgage financing in Denver, CO, requires a specialized approach. Unlike purchasing a single-family home, buying a condominium means your lender must approve both you as the borrower and the condo project itself. At Mortgage Maestro, a veteran-owned independent broker, we specialize in navigating the complexities of condo loans to help you secure the keys to your new property.

The most critical factor in condo financing is determining whether the community is warrantable or non-warrantable. A warrantable condo meets the strict guidelines set by Fannie Mae and Freddie Mac. This means the property is eligible for standard financing options, such as a conventional fixed-rate mortgage. On the other hand, a non-warrantable condo falls outside these standard guidelines. This might happen if a single entity owns too many units, the homeowner association (HOA) is facing litigation, or a large portion of the building is dedicated to commercial space.

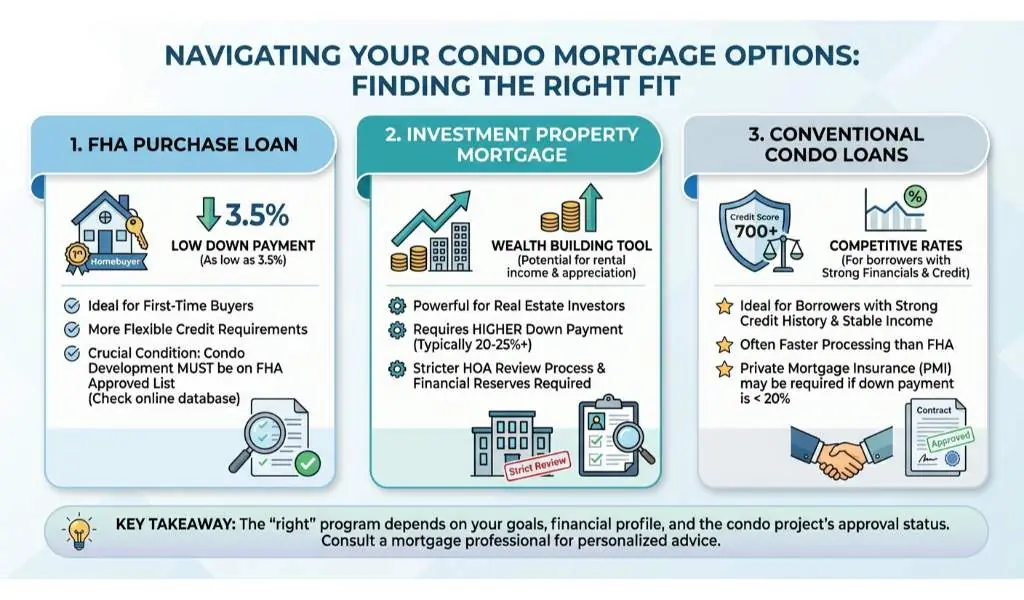

Exploring Your Condo Mortgage Options

Finding the right loan program is essential when exploring your condo mortgage options. If you are a first-time homebuyer or looking for a lower down payment, an FHA purchase loan might be an excellent fit, provided the condo development is on the FHA approved list. For those looking to build wealth through real estate, an investment property mortgage is a powerful tool, though it often requires a higher down payment and stricter HOA review.

- Conventional Condo Loans: Ideal for borrowers with strong credit looking to buy a warrantable condo.

- FHA Condo Loans: Great for buyers who need flexible credit requirements.

- Portfolio Loans: Often used for non-warrantable condos where standard guidelines do not apply.

Because the rules surrounding condo approvals are complex, working with an expert Denver mortgage broker is crucial. We are experts at providing second opinions on condo financing to ensure you are getting the best possible terms.

| Feature | Warrantable Condo | Non-Warrantable Condo |

|---|---|---|

| Lender Approval | Meets Fannie Mae and Freddie Mac guidelines | Does not meet standard agency guidelines |

| Commercial Space | Typically under 35 percent of total square footage | Often exceeds 35 percent commercial space |

| Investor Concentration | Majority of units are owner-occupied | High percentage of units are rented out |

| Financing Options | Conventional, FHA, VA loans | Portfolio loans, specialized non-QM loans |

| Interest Rates | Standard market rates | Typically slightly higher rates |

Why You Need a Second Opinion on Your Condo Loan

Have you been denied a condo loan by another lender? Do not give up just yet. We highly recommend getting a second opinion. Many large banks and retail lenders have internal overlays (extra rules) that make it difficult to approve condo mortgage financing. As an independent broker, Ray Williams and the team at Mortgage Maestro have access to a vast network of wholesale lenders.

We can often find solutions for properties that other lenders reject, especially when dealing with non-warrantable condo loans. Whether you are buying a downtown Denver high-rise or a quiet suburban townhome, a free second opinion could save you thousands of dollars and rescue your real estate transaction. Reach out to us at 303.779.0591 to discuss your scenario with a local expert.

Q1: What is a warrantable condo?

A warrantable condo is a property that meets the lending guidelines of government-sponsored enterprises like Fannie Mae and Freddie Mac. This makes it eligible for standard conventional financing.

Q2: Can I get an FHA loan for a condo in Denver?

Yes, you can get an FHA loan for a condo, but the entire condominium project must be approved by the Federal Housing Administration. If it is not on the approved list, your lender might be able to request a single-unit approval.

Q3: Why is condo financing more complicated than a standard home loan?

Condo mortgage financing requires the lender to evaluate the financial health of the homeowner association (HOA), the building’s insurance coverage, and the ratio of owner-occupied units to rentals.

Q4: Do I need a special loan for an investment condo?

Yes, purchasing a condo as a rental property typically requires an investment property mortgage. These loans generally require a larger down payment and have stricter qualification standards compared to primary residence loans.

Q5: Why should I get a second opinion on my condo mortgage?

Different lenders have different rules. If one lender denies your condo loan due to strict internal guidelines, an independent mortgage broker like Mortgage Maestro can often find another lender willing to approve the property.