Why Assumable Mortgages Are Denver’s Best Kept Real Estate Secret

If you are exploring the Denver real estate market in 2026, you have likely noticed that interest rates are looking vastly different than they did just a few years ago. But what if you could step into a seller’s shoes and take over their 3% interest rate? This is the magic of an assumable mortgage. At Mortgage Maestro Group, your trusted veteran-owned mortgage broker in Denver, CO, we are helping savvy buyers navigate this unique financing strategy.

An assumable mortgage allows a homebuyer to take over the seller’s existing loan terms, including the remaining balance, repayment schedule, and most importantly, the original interest rate. In a higher-rate world, assuming a loan from 2020 or 2021 can save you thousands of dollars annually.

Here are the primary benefits of pursuing an assumable loan in Colorado:

- Massive Interest Savings: Securing a rate in the 3% to 4% range instead of current market rates drastically lowers your monthly payment.

- Lower Closing Costs: Assuming a loan often requires fewer appraisal and origination fees compared to traditional financing.

- Competitive Edge: Sellers with assumable loans can market their homes at a premium, while buyers still walk away with an incredibly affordable monthly payment.

However, not all loans are assumable. Conventional loans rarely offer this feature. Instead, you will primarily be looking at government-backed loans like FHA, VA, and USDA loans. If you are a veteran, Ray Williams and our team can expertly guide you through the nuances of VA loan assumptions and entitlement transfers. Check out our loan options to see how these stack up against new financing.

The Process and Eligibility: How to Assume a Mortgage in Colorado

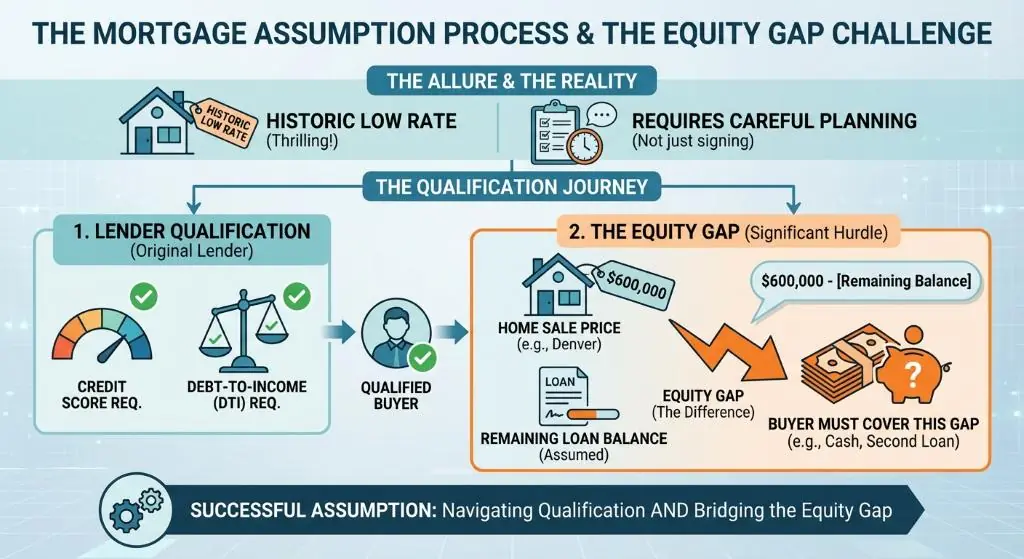

While the prospect of locking in a historic low rate is thrilling, the process requires careful planning. Assuming a mortgage is not as simple as signing a piece of paper. The buyer must still qualify for the loan with the seller’s original lender, meeting specific credit score and debt-to-income requirements.

The most significant hurdle buyers face is the equity gap. When you assume a mortgage, you only take over the remaining loan balance. If a home in Denver is selling for $600,000 and the assumable loan balance is $400,000, you must cover the $200,000 difference. You can bridge this gap through:

- Cash Reserves: Bringing your own funds to closing.

- A Second Mortgage: Taking out a secondary loan, though this will come at current market rates and must be approved by the primary lender.

- Seller Financing: The seller agrees to finance a portion of the equity gap.

So, when should you pursue an assumption versus applying for a completely new mortgage? An assumption makes sense if you have substantial cash on hand and the interest rate differential is large enough to offset the complex closing process. Conversely, if the seller has minimal equity or the lender’s assumption fees are exorbitant, a new loan might be faster and more practical. Our mortgage calculators can help you run the numbers on both scenarios.

| Loan Scenario (Based on $500,000 Loan) | Interest Rate | Monthly Principal & Interest | Total Interest Paid (Over 30 Years) |

|---|---|---|---|

| New 2026 Traditional Mortgage | 6.5% | $3,160 | $637,700 |

| Assumed 2021 FHA/VA Mortgage | 3.25% | $2,176 | $283,400 |

| Total Savings via Assumption | 3.25% Difference | $984 / month | $354,300 |

Navigating the Market with Mortgage Maestro Group

Finding a home with an assumable mortgage in Colorado requires a proactive approach and a knowledgeable team. Because real estate listings do not always explicitly advertise assumable loans, working with an experienced mortgage broker and real estate agent is essential. At Mortgage Maestro Group, led by Ray Williams, we pride ourselves on educating borrowers and finding creative financing solutions tailored to your unique financial goals.

We are the highest-rated independent mortgage broker in Denver, dedicated to taking the stress out of your home financing journey. Whether you are looking to assume a low-rate VA loan, explore conventional financing, or tap into your home equity, we offer more loan products than ever before.

Disclaimer: All loan approvals are subject to credit and underwriting approval. Interest rates and loan programs are subject to change without notice. Mortgage Maestro Group (NMLS #1838215) is an Equal Housing Lender serving Colorado, California, Florida, Wyoming, and Texas.

Ready to explore your options? Reach out for a free consultation today and let us help you build wealth through smart real estate financing.

Q1: What types of mortgages are assumable in Colorado?

FHA, VA, and USDA loans are generally assumable. Most conventional loans have a due-on-sale clause, making them non-assumable.

Q2: Do I need to be a veteran to assume a VA loan?

No, non-veterans can assume a VA loan. However, the seller’s VA entitlement will remain tied to the property until the loan is paid off, which may affect the seller’s ability to get another VA loan.

Q3: How long does the mortgage assumption process take?

The assumption process typically takes longer than a traditional mortgage closing, often ranging from 45 to 90 days, because it must go through the seller’s original lender.

Q4: Can I finance the equity gap when assuming a mortgage?

Yes, you can potentially take out a second mortgage to cover the difference between the home’s purchase price and the assumed loan balance, provided the primary lender allows it and you qualify.

Q5: Are there closing costs associated with assuming a mortgage?

Yes. While they are often lower than traditional closing costs, you will still need to pay an assumption fee, title insurance, and potential recording fees.