Smart Uses of Home Equity Without Increasing Monthly Stress

Vancouver homeowners are sitting on a goldmine. Over the past decade, property values across British Columbia have surged, leaving many families with substantial home equity. However, accessing this wealth often comes with a fear of skyrocketing monthly payments. At Pinsky Mortgages, we believe that tapping into your home’s value should alleviate financial pressure, not add to it.

Led by Vancouver mortgage expert Eitan Pinsky, our team has developed a sophisticated approach to equity optimization. Whether you are looking at a cash-out refinance, debt consolidation, or strategic home renovations, the goal is to protect your long-term affordability. Here are some of the smartest ways to leverage your equity:

- Debt Consolidation: Roll high-interest credit cards and personal loans into a lower mortgage rate to instantly improve cash flow.

- Value-Adding Renovations: Invest in secondary suites or modern upgrades that increase your property value and potential rental income.

- Strategic Investments: Use equity to fund a down payment on a rental property in BC, creating a new passive income stream.

By restructuring your finances correctly, you can unlock capital while maintaining or even reducing your total monthly financial obligations.

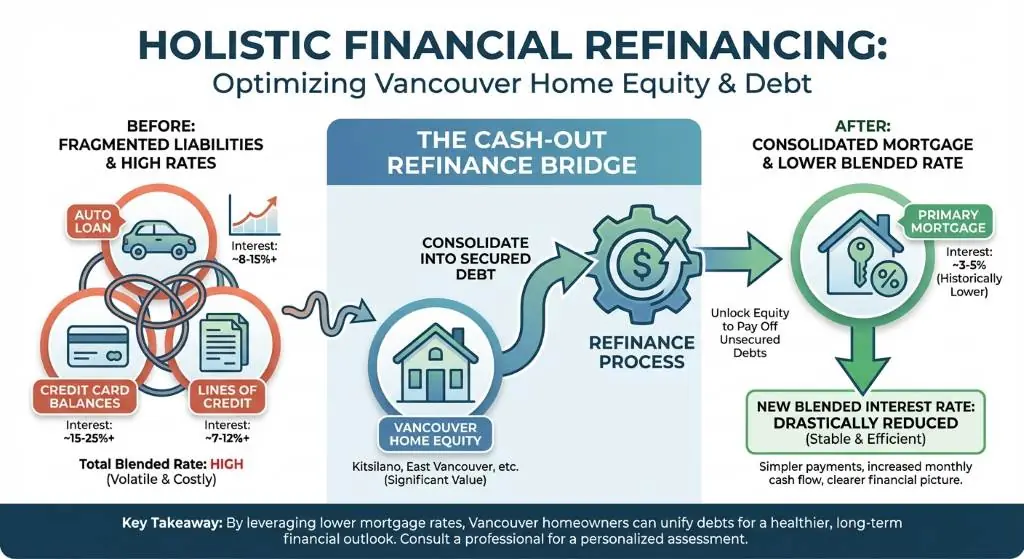

Navigating Cash-Out Refinancing and Debt Consolidation in Vancouver

When considering a cash-out refinance in Vancouver, the key is looking at your holistic financial picture. Many BC homeowners carry a mix of auto loans, credit card balances, and lines of credit. Because mortgage interest rates are historically much lower than unsecured debt, consolidating these liabilities into your primary mortgage can drastically reduce your blended interest rate.

For example, if you have built up significant equity in your Kitsilano or East Vancouver home, you can refinance to pay off a 19% interest credit card. The result is a single, manageable monthly payment. This strategy is not about taking on more debt; it is about optimizing the debt you already have. Working with a local expert like Eitan Pinsky ensures you find the right lender and product, whether that is a Home Equity Line of Credit (HELOC) or a traditional mortgage refinance.

| Debt Type | Current Balance | Interest Rate | Current Monthly Payment | New Consolidated Payment (Estimated) |

|---|---|---|---|---|

| Credit Cards | $25,000 | 19.99% | $750 | Included in Mortgage |

| Auto Loan | $35,000 | 8.50% | $650 | Included in Mortgage |

| Personal Line of Credit | $15,000 | 10.00% | $300 | Included in Mortgage |

| Total Before Consolidation | $750,000 (Mortgage) + $75,000 | Mixed | $5,200 | N/A |

| Total After Refinance | $825,000 | 5.00% (Example) | N/A | $4,800 (Total Savings: $400/mo) |

Funding Home Renovations While Protecting Long-Term Affordability

Another highly effective way to use your home equity is through strategic renovations. In the competitive BC real estate market, adding a laneway house or a basement suite can dramatically increase your property value while generating steady rental income. This income can often offset the cost of the borrowed equity, making the renovation essentially pay for itself.

Before you swing a hammer, it is crucial to consult with a mortgage professional. At Pinsky Mortgages, we guide Vancouver homeowners through construction mortgages and renovation financing options. We help you calculate the projected return on investment to ensure that borrowing against your home does not compromise your long-term financial stability. By optimizing your equity smartly, you can upgrade your living space, increase your net worth, and keep your monthly stress levels low.

Q1: What is equity optimization?

Equity optimization is the strategic process of using your home’s accumulated value to improve your overall financial position, such as consolidating high-interest debt or funding value-adding renovations, without causing undue monthly financial stress.

Q2: Can I access my home equity without refinancing my current mortgage?

Yes, homeowners in BC can often access their equity through a Home Equity Line of Credit (HELOC) or a second mortgage. These options allow you to tap into your home’s value while keeping your primary mortgage rate and terms intact.

Q3: How does debt consolidation using home equity lower my monthly payments?

By rolling high-interest debts like credit cards and car loans into your mortgage, you take advantage of significantly lower interest rates. This extends the repayment term for those debts and drastically reduces the total amount you pay each month.

Q4: Is it a good idea to use home equity for renovations in Vancouver?

Using equity for renovations is highly recommended if the upgrades add tangible value to your property or generate rental income, such as building a secondary suite. This strategy can yield a strong return on investment in the Vancouver housing market.

Q5: How can Pinsky Mortgages help me optimize my home equity?

Led by Eitan Pinsky, our Vancouver-based team analyzes your complete financial profile to recommend the best equity extraction strategies. We negotiate with lenders to secure favorable rates and terms that align with your long-term affordability goals.