What is an FHA Loan and How Can It Help You Buy a Home?

If you are dreaming of owning a home in the beautiful city of Denver, CO, but feel overwhelmed by the strict requirements of traditional financing, an FHA loan might be your perfect solution. An FHA purchase loan is a mortgage insured by the Federal Housing Administration. This government backing allows lenders to offer more flexible qualification requirements, making it an incredibly popular choice for many buyers.

One of the biggest hurdles to homeownership is saving for a massive down payment. With FHA loans, you can secure a home with as little as 3.5% down. This makes it an outstanding option if you are exploring a first-time homebuyer mortgage. Unlike a conventional fixed-rate mortgage, which often requires a higher credit score and larger down payment, the FHA purchase loan is designed to be accessible to a wider range of buyers.

At Mortgage Maestro, we specialize in helping Denver residents navigate their home financing options. Whether you are just starting your journey or looking for a trusted expert to review your current pre-approval, we are here to help. In fact, we are experts at providing second opinions on FHA purchase loans to ensure you are getting the absolute best terms for your financial future.

FHA Loan Options and Qualification Requirements

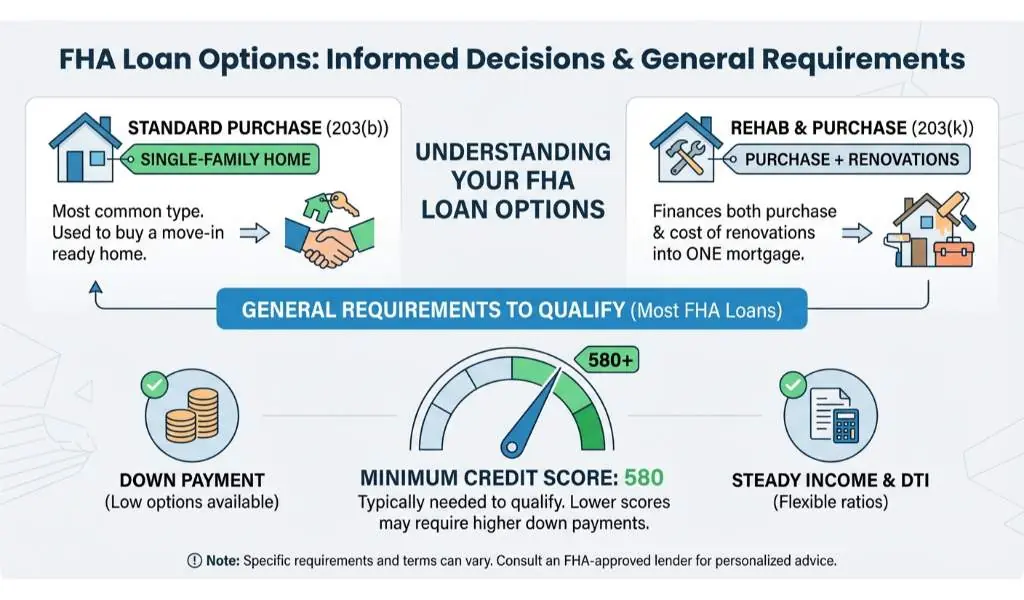

Understanding your FHA loan options is crucial for making an informed financial decision. The standard FHA purchase loan, known as the 203(b) loan, is the most common type used to buy a single-family home. However, there are also options like the 203(k) rehab loan, which allows you to finance both the purchase and the cost of renovations into a single mortgage.

Here are the general requirements to qualify for most FHA loans:

- Credit Score: A minimum score of 580 is typically needed to qualify for the low 3.5% down payment advantage.

- Debt-to-Income Ratio: Lenders prefer a DTI ratio under 43%, though exceptions exist for borrowers with compensating factors.

- Property Standards: The home must meet specific safety and structural guidelines set by the FHA.

- Steady Income: You will need to provide proof of consistent employment and income.

If you are an eligible military member or veteran, you might also want to compare these benefits with a VA purchase loan, which offers zero down payment options. If you already have an offer from another lender, do not hesitate to reach out to us. We highly recommend getting a free second mortgage opinion. It could save you thousands over the life of your loan, and we pride ourselves on delivering honest, transparent feedback on your FHA loan terms.

| Loan Feature | FHA Loan | Conventional Loan | VA Loan |

|---|---|---|---|

| Minimum Down Payment | 3.5% | 3% to 5% | 0% |

| Minimum Credit Score | 580 (for 3.5% down) | 620 | No official minimum (often 580+) |

| Mortgage Insurance | Upfront and Annual MIP | PMI (if under 20% down) | No PMI (Funding Fee applies) |

| Best For | Buyers with lower credit or smaller down payments | Buyers with strong credit and larger down payments | Eligible Veterans and Active Military |

Why Choose Mortgage Maestro for Your Denver FHA Loan?

Choosing the right mortgage broker is just as important as choosing the right home. As a top-rated, veteran-owned independent mortgage broker in Denver, CO, Mortgage Maestro is dedicated to educating borrowers and finding the perfect loan products for their unique situations. We understand the local Colorado real estate market and work tirelessly to ensure your financing journey is smooth and stress-free.

When you work with Ray Williams and our dedicated team, you are not just getting a loan. You are gaining a financial partner. We leverage industry-leading technology to explain every detail of your FHA purchase loan, ensuring you feel confident at the closing table. Remember, if you are currently under contract or pre-approved elsewhere, we are experts at providing second opinions on FHA purchase loans. A quick review of your Loan Estimate by our team could reveal better rates or significantly lower fees.

Compliance Note: Mortgage Maestro is an Equal Housing Opportunity broker. NMLS#1838215. All loan approvals are subject to credit and underwriting approval.

Q1: What is the maximum loan amount for an FHA loan in Denver, CO?

FHA loan limits vary by county and change annually. For the Denver metro area, the limits are generally higher to accommodate the local housing market. Contact us for the most up-to-date figures.

Q2: Can I use gift funds for my FHA loan down payment?

Yes. FHA guidelines allow you to use 100% gift funds for your down payment and closing costs, provided the gift comes from an approved source like a family member.

Q3: Do FHA loans require mortgage insurance?

Yes, FHA loans require both an Upfront Mortgage Insurance Premium (UFMIP) and an annual premium paid monthly. This insurance is what allows lenders to offer such favorable terms.

Q4: How long does it take to close an FHA purchase loan?

On average, it takes about 30 to 45 days to close an FHA loan. Our team at Mortgage Maestro works efficiently to ensure a fast, on-time closing.

Q5: Why should I get a second opinion on my FHA loan?

Different lenders offer varying rates and fees. Getting a free second opinion from our experts ensures you are not overpaying and that you are receiving the best possible FHA purchase loan terms available.

Call Ray Williams at 303.779.0591 for a Free FHA Loan Consultation!