Understanding First-Time Buyer Loans and Your Options

Buying your first home in Denver is an exciting milestone, but navigating the world of real estate financing can feel overwhelming. Securing the right first time homebuyer mortgage is the foundation of a successful purchase. At Mortgage Maestro, a veteran-owned independent mortgage broker, we specialize in helping Colorado residents find the perfect financing solutions.

Whether you are exploring traditional conventional loans or looking into an FHA purchase loan, understanding your options is crucial. Many buyers are surprised to learn they do not need a 20 percent down payment. In fact, numerous down payment assistance programs and specialized first-time buyer loans can make homeownership highly accessible.

- Expert Guidance: We simplify the complex lending process.

- Second Opinions: Already have a quote? We are experts at providing second opinions on first-time homebuyer mortgages to ensure you get the absolute best deal.

- Local Knowledge: We know the Denver market inside and out.

HomeReady and Home Possible: Top First-Time Home Buyer Mortgage Programs

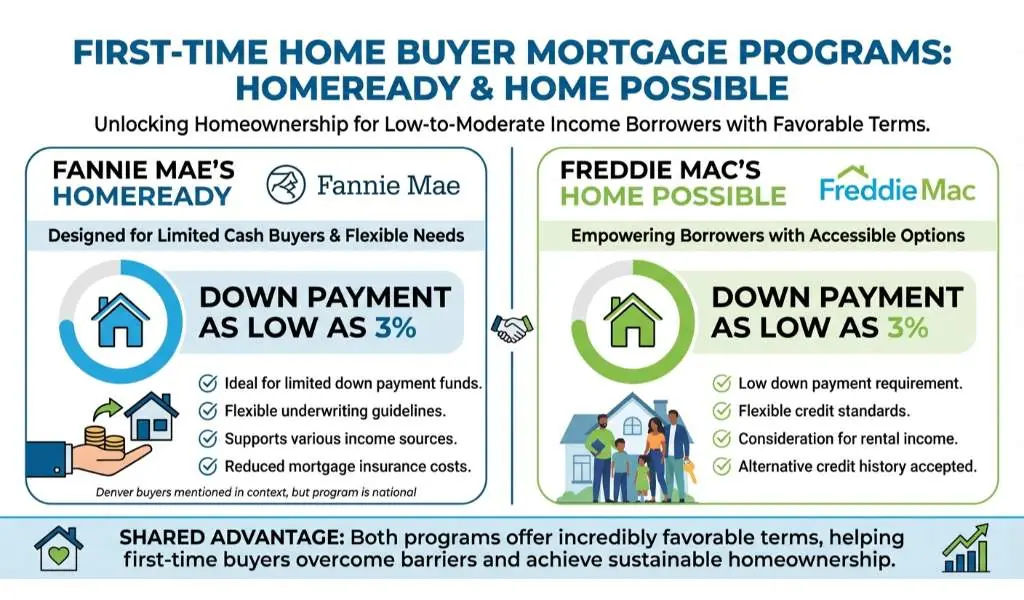

When exploring a first-time home buyer mortgage, two of the most popular and advantageous programs available are Fannie Mae’s HomeReady and Freddie Mac’s Home Possible. Both are designed to help low to moderate-income borrowers achieve homeownership with incredibly favorable terms.

HomeReady by Fannie Mae

The HomeReady program is fantastic for Denver buyers who might have limited cash for a down payment. It allows for a down payment as low as 3 percent. Additionally, it offers flexible underwriting, meaning you can use income from non-borrower household members to help you qualify. This is a brilliant solution for multi-generational families living under one roof.

Home Possible by Freddie Mac

Similarly, the Home Possible program offers a 3 percent down payment option but caters slightly differently to borrowers. It is highly beneficial for those who might need to use sweat equity (repairs or improvements made by the borrower) toward their down payment and closing costs.

Both programs offer reduced mortgage insurance premiums compared to standard conventional loans, keeping your monthly payments lower. As your trusted Denver mortgage broker, Ray Williams and the team at Mortgage Maestro will evaluate your unique financial situation to determine which of these first-time buyer loans suits you best.

| Feature | HomeReady (Fannie Mae) | Home Possible (Freddie Mac) | FHA Loan |

|---|---|---|---|

| Minimum Down Payment | 3% | 3% | 3.5% |

| Minimum Credit Score | Typically 620 | Typically 660 | 580 (for 3.5% down) |

| Income Limits | 80% of Area Median Income (AMI) | 80% of Area Median Income (AMI) | No income limits |

| Mortgage Insurance | Reduced, cancelable at 20% equity | Reduced, cancelable at 20% equity | Required for the life of the loan (usually) |

Why You Should Get a Second Opinion on Your Mortgage Quote

Many prospective homeowners accept the very first loan estimate they receive. However, getting a second opinion on your first time homebuyer mortgage can save you thousands of dollars over the life of your loan. At Mortgage Maestro, we pride ourselves on providing comprehensive second opinions for Denver buyers.

Even a fraction of a percent difference in your interest rate or lower closing costs can make a massive financial impact. We review your current offer and compare it against our extensive portfolio of loan products. If you already have a great deal, we will tell you. If we can beat it, we will show you exactly how much you can save.

Remember, working with an independent, veteran-owned broker means we work for you, not the bank. We have access to diverse lenders, ensuring your first-time home buyer mortgage is perfectly tailored to your long-term financial goals.

Q1: What qualifies me as a first-time homebuyer in Denver?

Generally, if you have not owned a principal residence in the past three years, lenders consider you a first-time homebuyer. This status opens up access to specific first-time buyer loans and down payment assistance programs.

Q2: Can I buy a home with no down payment?

While most conventional and FHA loans require a small down payment of 3% to 3.5%, qualifying veterans can use a VA loan for zero down. Additionally, pairing a standard loan with down payment assistance programs can help cover the upfront costs.

Q3: What credit score do I need for a first-time homebuyer mortgage?

Credit score requirements vary by loan type. FHA loans often accept scores as low as 580, while conventional programs like HomeReady typically require a score of 620 or higher.

Q4: Is it worth getting a second opinion on my mortgage offer?

Absolutely. We are experts at providing second opinions on first-time homebuyer mortgages. Comparing offers can reveal hidden fees or secure a lower interest rate, saving you significant money over time.

Q5: How long does the pre-approval process take?

At Mortgage Maestro, we strive for fast and efficient service. Once you provide the necessary financial documents, we can often issue a pre-approval within 24 to 48 hours to help you start house hunting in Denver immediately.

Ready to Secure Your Dream Home in Denver?

Contact Ray Williams at Mortgage Maestro today for a free consultation or an expert second opinion on your mortgage.