The Advanced Affordability Math for Denver Homebuyers

When planning a home purchase in the Denver metro area, the focus often lands squarely on interest rates and home prices. However, a new financial reality is taking center stage for 2026. Homebuyers must now account for a crescendo of rising insurance premiums, property taxes, and Homeowner Association (HOA) dues. As a trusted Denver mortgage broker, Mortgage Maestro Group is helping clients understand this advanced affordability math. The hidden costs of homeownership are shifting debt-to-income ratios and altering purchasing power across the Front Range.

Several factors are driving these increases:

- Wildfire and Flood Risks: Changing climate models have prompted insurance carriers to drastically increase premiums or pull out of certain high-risk zip codes entirely.

- Rising Millage Rates: Local municipalities are adjusting property tax rates to fund essential services, directly impacting your monthly escrow requirements.

- HOA Reserve Replenishment: Many communities are raising dues to cover their own skyrocketing master insurance policies and deferred maintenance.

Understanding these variables early is critical. You can explore our loan options to see how different mortgage structures might help absorb some of these localized costs.

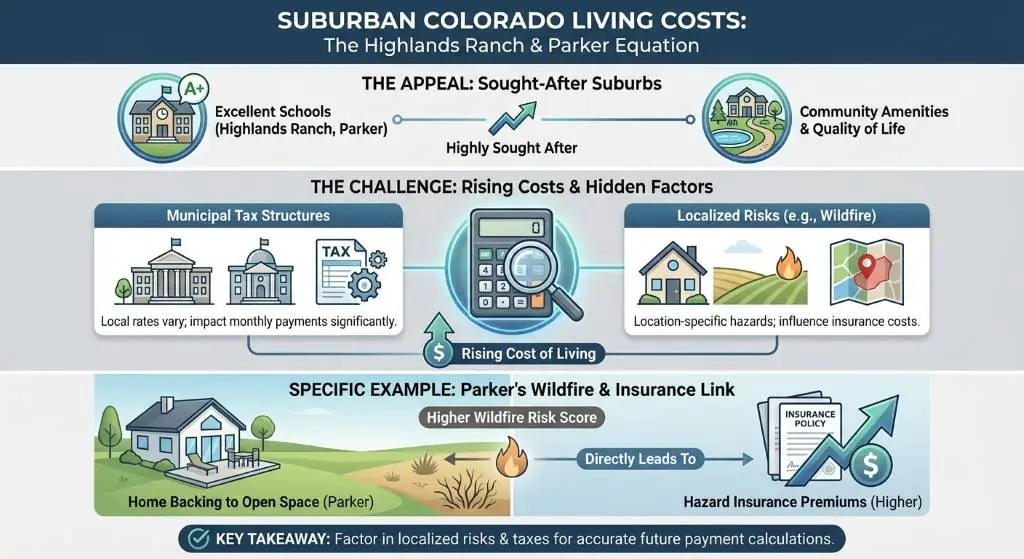

How Wildfire Risks and Rising Millage Rates Shift Buying Power

Suburbs like Highlands Ranch and Parker are highly sought after for their excellent schools and community amenities. Yet, these areas are not immune to the rising costs associated with suburban Colorado living. When you sit down to calculate your future payments, you must factor in the specific localized risks and municipal tax structures.

For example, homes backing up to beautiful open spaces in Parker may carry a higher wildfire risk score. This can lead to hazard insurance premiums that are double or triple what they were just three years ago. Similarly, Highlands Ranch homeowners are seeing HOA dues increase as community management boards face their own rising insurance and maintenance costs. These hidden notes in your housing payment directly impact your debt-to-income ratio, which dictates how much house you can qualify for.

To stay ahead of the curve, we highly recommend using our mortgage calculators to run scenarios that include inflated tax and insurance estimates. As an independent, veteran-owned brokerage, Ray Williams and the team at Mortgage Maestro Group will help you navigate these complex local variables.

| Expense Category (Estimated for $600k Home) | 2023 Average Monthly Cost | Projected 2026 Monthly Cost | Impact on Buying Power |

|---|---|---|---|

| Hazard Insurance (Wildfire Risk Zones) | $150 | $350+ | Moderate to High |

| Property Taxes (Rising Millage) | $300 | $425 | High |

| HOA Dues (Suburbs like Highlands Ranch) | $65 | $110 | Low to Moderate |

Strategizing Your 2026 Colorado Home Purchase

Navigating the 2026 housing market requires a proactive approach. You cannot afford to wait until you are under contract to discover that a home’s insurance premium pushes you out of your qualification bracket.

Here are actionable steps to protect your homeownership goals:

- Shop Insurance Early: Ask your real estate agent for the Comprehensive Loss Underwriting Exchange (CLUE) report and get insurance quotes before making an offer.

- Review HOA Financials: Ensure the community you are buying into has a well-funded reserve. Underfunded HOAs are prime candidates for massive special assessments.

- Partner with a Local Expert: National call-center lenders often use generic estimates for taxes and insurance. A local expert knows exactly what to expect in Denver, Parker, and Highlands Ranch.

At Mortgage Maestro Group, we provide tailored advice that factors in every hidden note of your monthly payment. Ready to build a realistic, stress-free budget? Apply online today to get a comprehensive pre-approval.

Q1: How do rising property taxes affect my mortgage qualification in Colorado?

Property taxes are a key component of your monthly housing expense. When millage rates rise, your projected monthly payment increases, which raises your debt-to-income ratio and can lower the total loan amount you qualify for.

Q2: Why are hazard insurance premiums increasing so rapidly in areas like Parker?

Insurance carriers are updating their risk models to account for increased wildfire and severe weather threats. Homes near open spaces or in designated fire zones face higher premiums as companies mitigate their potential losses.

Q3: Can high HOA fees in Highlands Ranch prevent me from getting a mortgage?

Yes, HOA fees are included in your debt-to-income calculation. If a community has exceptionally high dues or pending special assessments, it could push your financial ratios above the limits allowed by lenders.

Q4: What is the benefit of using an independent Denver mortgage broker like Mortgage Maestro Group?

As a local, veteran-owned brokerage, we have access to a wide variety of wholesale lenders. We understand local tax rates and insurance challenges, allowing us to find flexible loan options that national banks might miss.

Q5: When should I start getting insurance quotes during the home buying process?

You should start requesting preliminary insurance quotes as soon as you identify a property you want to bid on. Knowing the exact insurance costs beforehand ensures your mortgage pre-approval remains valid.