Understanding the 2026 Renewal Wave and Fed Stability

The Denver real estate market is bracing for a significant shift as we approach the 2026 renewal wave. For many Colorado homeowners who secured short-term adjustable-rate mortgages or are facing the maturation of low-rate loans, the impending adjustments could lead to a steep increase in monthly housing costs. However, with strategic planning and the guidance of a trusted Denver mortgage broker, you can navigate this landscape to potentially cut your payments by $400 or more per month.

As the Federal Reserve maintains a stance of stability, the window for optimal timing is opening. Homeowners must look beyond simply waiting for rates to drop and instead focus on proactive financial modeling. By partnering with a veteran-owned independent broker like Ray Williams at Mortgage Maestro, you can evaluate your current loan options and implement a refinance strategy before rates shift unfavorably.

- Maturing Low-Rate Loans: Prepare for the end of your introductory rate period before your payments spike.

- Fed Stability: Capitalize on the current predictable market conditions to lock in a secure financial path.

- Proactive Refinancing: Execute a strategy now to lock in savings before the 2026 wave hits full force.

Breakeven Modeling and Blended Rates Explained

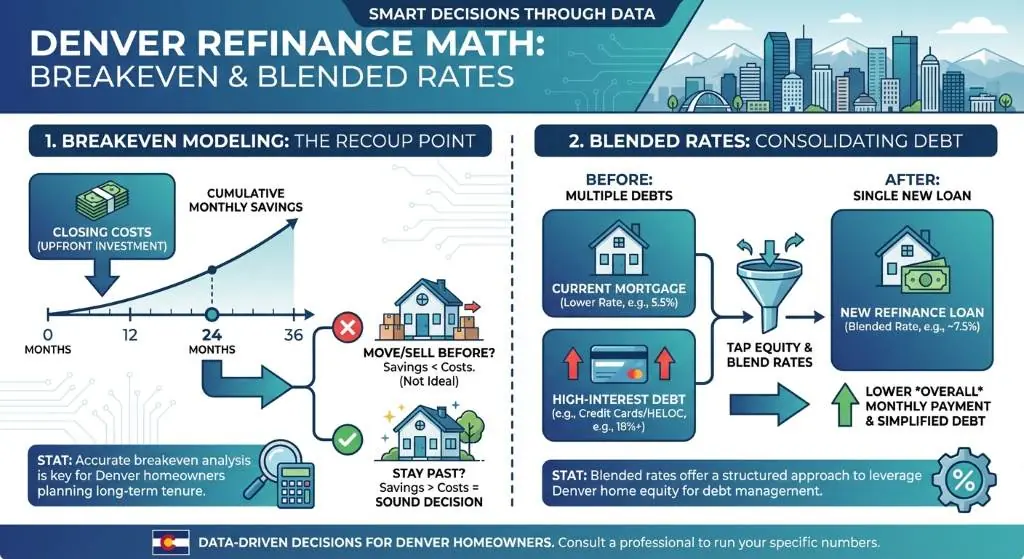

When considering a refinance in Denver, understanding the math behind your decision is crucial. This is where breakeven modeling and blended rates come into play. Breakeven modeling calculates exactly how many months it will take for your monthly savings to cover the closing costs of the new loan. If you plan to stay in your Denver home past this breakeven point, refinancing becomes a highly sound financial decision.

Additionally, if you are looking to tap into your home equity to consolidate debt, looking at your blended rate is essential. A blended rate combines the interest rate of your primary mortgage with the rate of your consumer debt, such as credit cards or auto loans. Even if a new mortgage rate is slightly higher than your current locked-in rate, the overall blended rate of your total debt can drop significantly. This strategy can easily save you upwards of $400 a month. You can use our mortgage calculators to start running these numbers yourself.

| Financial Metric | Current Loan Scenario | Proposed Refinance Strategy | Net Difference |

|---|---|---|---|

| Primary Mortgage Rate | 3.5% | 5.75% | +2.25% |

| High-Interest Debt | $35,000 at 22% | Consolidated into Mortgage | N/A |

| Total Monthly Payment | $3,250 | $2,825 | -$425 |

| Blended Interest Rate | 8.9% | 5.75% | -3.15% |

Optimal Timing: Why Denver Homeowners Should Act Now

The key to maximizing your savings during the 2026 Denver renewal wave is optimal timing. Waiting for the perfect, rock-bottom interest rate can be a costly mistake if your current low-rate loan matures in the meantime. By taking a proactive approach to your mortgage refinance, you secure financial peace of mind and protect your household budget from unexpected spikes.

Every homeowner has a unique financial fingerprint, which is why personalized advice is so valuable. Whether you are looking at debt consolidation, investor cash flow loans, or simply wanting to lower your monthly overhead, our top-tier mortgage brokering team is here to help. We proudly serve homeowners in Colorado, California, Florida, Wyoming, and Texas, offering more loan products than ever before. Let us help you build wealth and secure a stable future.

Q1: What is the 2026 Denver renewal wave?

It refers to the large number of short-term adjustable-rate mortgages and low-rate loans maturing around 2026, which may cause monthly payments to increase significantly for many Colorado homeowners.

Q2: How can I cut my mortgage payments by $400 or more?

By utilizing a strategic refinance that consolidates high-interest debt, you can lower your overall blended interest rate and significantly reduce your total monthly outgoing payments.

Q3: What does breakeven modeling mean in refinancing?

Breakeven modeling is a calculation that determines how many months it will take for your monthly mortgage savings to pay off the initial closing costs of the refinance.

Q4: Why should I work with an independent Denver mortgage broker?

An independent broker like Mortgage Maestro shops multiple lenders to find you the best rates and loan options, offering personalized advice tailored to your specific financial goals rather than a one-size-fits-all product.

Q5: Is now a good time to refinance if rates are higher than my current mortgage?

Yes, it absolutely can be. If you have significant high-interest consumer debt, refinancing to consolidate that debt can lower your blended rate and save you money every month, even if the primary mortgage rate is slightly higher.

Schedule Your Free Refinance Consultation with Ray Williams Today