In recent years, American seniors contributed significantly to the Reverse Mortgage Loans market, surpassing $6 billion in total—a 30% increase from the previous year. This growth highlights an increasing trend among seniors to utilize home equity for retirement funding.

Additionally, many American seniors prefer to remain in their homes instead of downsizing, viewing it as essential for maintaining independence and comfort during their retirement years. This preference has led to a surge in seniors opting for Reverse Mortgage Loans, choosing this method as a favorable alternative to traditional retirement savings plans.

What is a Reverse Mortgage Loans?

A Reverse Mortgage Loan is a specialized loan available to homeowners aged 62 or older, enabling them to transform a portion of their home equity into cash. This financial tool is particularly beneficial for covering vital living expenses or healthcare costs without the burden of monthly repayments.

The loan does not require repayment until the homeowner relocates, sells their property, or passes away. Additionally, it offers a way for seniors to remain in their homes while accessing the equity they have built up over the years, thus providing both financial relief and stability in retirement.

Types of Reverse Mortgage Loans

Reverse Mortgage Loans offer a way for seniors to access the equity in their homes without the obligation of monthly payments. These loans come in various forms, each designed to meet different needs and circumstances. Here are the types of Reverse Mortgage Loans available:

Single-purpose Reverse Mortgage Loans

These are niche products designed to help homeowners meet specific financial challenges, such as paying for home repairs, property taxes, or other approved expenses. Offered mainly by state and local government agencies or non-profit organizations, these loans are typically less costly and have fewer fees than other Reverse Mortgage Loans.

The limited scope of their use often makes them less versatile but more accessible for those who meet the criteria.

Proprietary Reverse Mortgage Loans

Tailored for homeowners with higher-value properties, proprietary Reverse Mortgage Loans are private loans not insured by the federal government. These can provide larger loan amounts than

Important Considerations

Costs

Reverse Mortgage Loans typically involve several fees and charges that can affect the total cost of the loan. These fees include mortgage insurance premiums, which protect the lender in case the home’s sale does not cover the full loan balance upon the borrower’s passing or move-out.

Additionally, loan origination fees cover the lender’s administrative costs. Both are generally deducted from the total loan amount, reducing the cash available to the borrower. Ongoing costs may also include annual mortgage insurance premiums and loan servicing fees.

Impact on Inheritance

A significant concern with Reverse Mortgage Loans is their impact on the borrower’s estate and heirs. If the heirs wish to keep the property, they must pay off the Reverse Mortgage Loan balance, potentially using other funds or refinancing into a traditional mortgage.

Financial Counseling

Before securing a Reverse Mortgage Loan, it’s beneficial to consult with a financial advisor or a counselor. Speaking with a knowledgeable advisor can help homeowners understand the long-term implications and suitability of a Reverse Mortgage Loan in their financial situation.

This guidance is vital in helping borrowers and their families make informed decisions that align with their financial goals and needs.

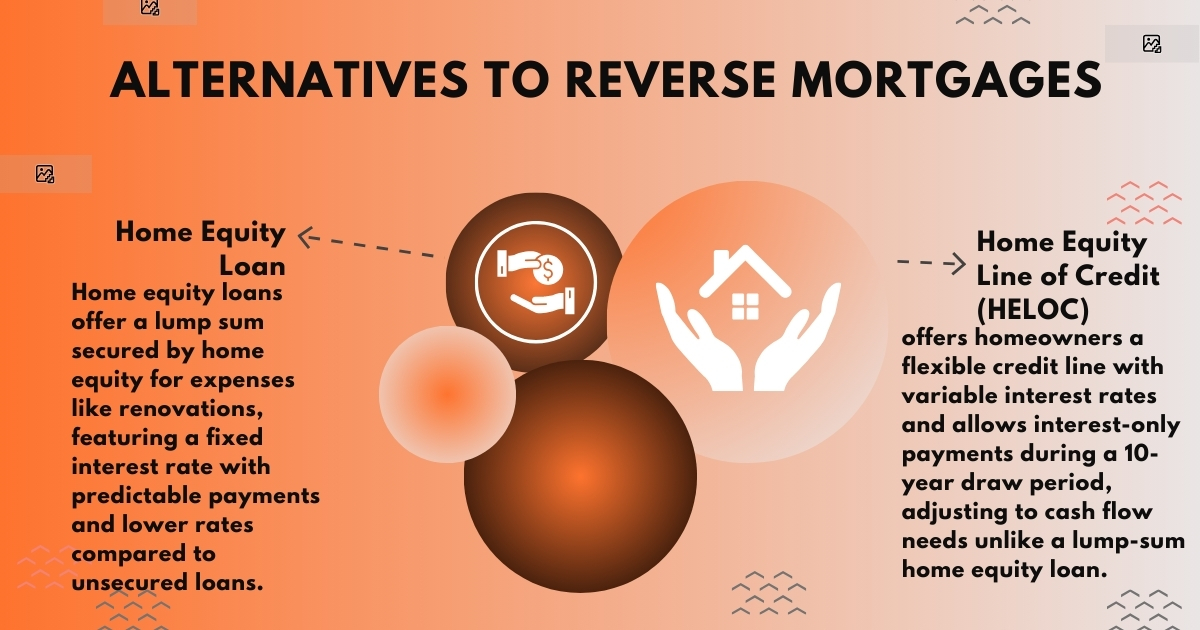

Alternatives to Reverse Mortgage Loans

Home Equity Loans

These loans are secured by the equity in your home, providing a one-time lump sum that homeowners can use for large expenses such as home renovations, consolidating debt.

The key feature of a home equity loan is its fixed interest rate, which offers predictability in budgeting since the monthly payments remain the same throughout the term of the loan.

Home Equity Line of Credit (HELOC)

Unlike a home equity loan that disburses a lump sum, a HELOC provides a credit line that homeowners can draw from as needed, much like a credit card but with a much larger available balance.

This option offers flexibility in borrowing and repaying funds according to the homeowner’s cash flow needs. Interest rates on HELOCs are variable, which means they can fluctuate with the market conditions, potentially affecting monthly payments.

During the draw period, which is typically 10 years, borrowers can withdraw funds up to their credit limit and may have the option to make interest-only payments.

Both options use the homeowner’s equity as collateral and thus require careful consideration to ensure that the added debt does not overextend the homeowner’s financial capabilities.

Your Financial Freedom with Mortgage Maestro Group

Considering a Reverse Mortgage Loan? Join American seniors who have found financial relief and maintained independence by tapping into their home equity. Mortgage Maestro Group stands out as your best choice, offering expert guidance and personalized solutions.

Trust us to help you navigate your options safely and effectively, ensuring you make the most out of your home’s value. Connect with Mortgage Maestro Group today and start your journey towards a secure financial future in the comfort of your home.

Final Thoughts

As more American seniors choose Reverse Mortgage Loans, it becomes clear that this option is more than just a financial strategy—it’s a way to stay independent and comfortable in retirement. Reverse Mortgage Loans allow seniors to access their home equity to manage expenses without monthly payments.

As interest in this option grows, it’s beneficial for anyone considering a Reverse Mortgage Loan to seek advice and fully understand the financial impact to ensure it fits their long-term retirement plans. To talk further about your needs, or your family member needs send us a note and we’ll call to discuss if a Reverse Mortgage Loan is right for your situation.

FAQs

How does a Reverse Mortgage Loan work in Colorado?

A Reverse Mortgage Loan in Colorado allows homeowners aged 62 or older to convert part of their home equity into cash while retaining ownership. The loan amount is based on the home’s equity, the borrower’s age, and current interest rates.

What does it mean when you do Reverse Mortgage Loans?

Taking out a Reverse Mortgage Loan means receiving a loan against the equity of your home, without the obligation of monthly payments. Instead, the loan accrues interest and is repaid when you sell the home, move out permanently, or die.

It allows homeowners to access their built-up home equity and use it for expenses such as healthcare or living costs.

What is the difference between a reverse mortgage loan and a reverse purchase?

A Reverse Mortgage Loan allows you to borrow against the equity of your current home, converting it into cash. In contrast, a reverse purchase involves using a reverse mortgage loan to buy a new home.

This helps seniors purchase a new primary residence without having to make monthly mortgage payments, simplifying the transition to a new home suitable for their retirement.

What is the difference between a reverse mortgage loan and a second mortgage?

A Reverse Mortgage Loan does not require monthly payments and is repaid when the homeowner dies, sells, or permanently moves out.

Mortgage Maestro Group – NMLS #1838215